We’re always looking for ways to intentionally lower our expenses which is one of the reasons tax planning has caught my interest.

I know it sounds boring AF, but when you realize that the biggest area you spend money in is actually your taxes, you may change your mind.

The average American spends 40-50% of their income on taxes 🤯

So a high-impact way to increase the money you have is to reduce what you have to pay in taxes. This is especially important for those of you in higher income brackets.

There are many ways to do this, but today we’re going to talk about tax-loss harvesting, because the end of the year is coming up and this strategy can give you some quick wins.

Podcast Episode

If reading isn’t your thing, you can watch Episode 82 of our podcast or listen on your favorite podcast platform.

What is Tax-Loss Harvesting

Tax-loss harvesting is a strategy that can be used to lower your taxable income by intentionally selling an investment for a loss to offset the taxable gains of another investment.

It can be done at any time during the year even though you usually hear about it in December.

What’s even cooler is, if your losses are larger than your gains, you can also reduce your ordinary income that can be taxed by up to $3,000 (1,500 if married and filing separately).

Talk about a great way to keep more of your money and the dividend compounding machine throttled to the max.

Who Is Tax-Loss Harvesting For?

Tax-loss harvesting won’t benefit everyone, so first let’s make sure that you can take advantage of this nifty strategy.

☑️ Investors Who Use A Taxable Brokerage Account

Many people invest through their employer. If all of your investments are in retirement accounts, you aren’t eligible to use tax-loss harvesting because you’re already getting a tax benefit. The IRS don’t do double dippin’.

You must have a taxable brokerage account to use this strategy.

☑️ Investors Who Sell Their Stocks

If your investing strategy is to keep buying and holding for the long haul, you won’t have any realized gains to offset.

The IRS doesn’t consider your gains to be “real” (taxable) until you sell your assets. In order to take advantage of tax-loss harvesting you need to have realized gains in your portfolio and be willing to sell to lock in realized losses.

If you use our value investing strategy to buy stocks that are undervalued and sell when they’re overvalued, you’ll have realized gains to offset.

☑️ Investors Who Are In Higher Income Brackets

If your income puts you in the higher tax brackets, or some of it bleeds into one that’s a 8-10% jump up, you’ll love what tax-loss harvesting can do for you.

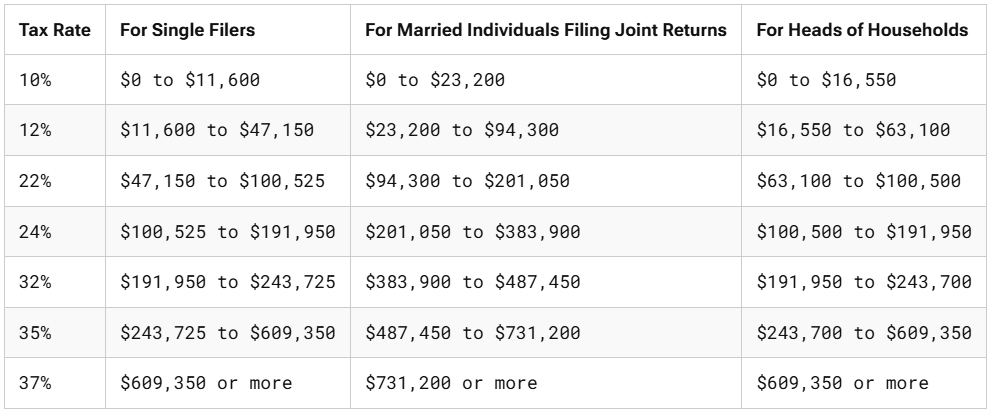

Let’s say you made $94,300 in income. Using 2024’s Federal Tax Brackets, you’d pay 12% tax on the first $47,150 ($5,658) and 22% tax on the other $47,150 ($10,373).

Notice how you’re paying a higher proportion to taxes on money in the higher bracket. Therefore, any money you offset in higher brackets will give you more bang for your bucks.

Who Is Tax-Loss Harvesting Not For

Again, make sure your situation doesn’t DQ you from using this strategy before you sell anything.

✖️ Investors Who Only Have Retirement Accounts

If you only have investments in tax-advantaged accounts, you’re already getting a tax benefit by either deferring taxes until you withdraw money or by paying taxes up front and never paying them again.

You cant do tax-loss harvesting in the following accounts. This is not an all-inclusive list.

- IRAs

- 401(k)s

- Health Savings Accounts (HSAs)

- 529s

- SEPs

- Flexible Spending Accounts

✖️ Investors Who Don’t Sell Their Stocks

Many investing strategies revolve around buying and holding for the long term.

- Boggleheads with their index funds

- People who use Term-Date Funds

- Total market ETFs or mutual funds

- Long term growth investors

- Dividend investors who don’t sell

You have to buy and sell stocks in a given tax year to be able to harvest any tax-losses. If any of the above is you, you need to focus on other ways to save on taxes.

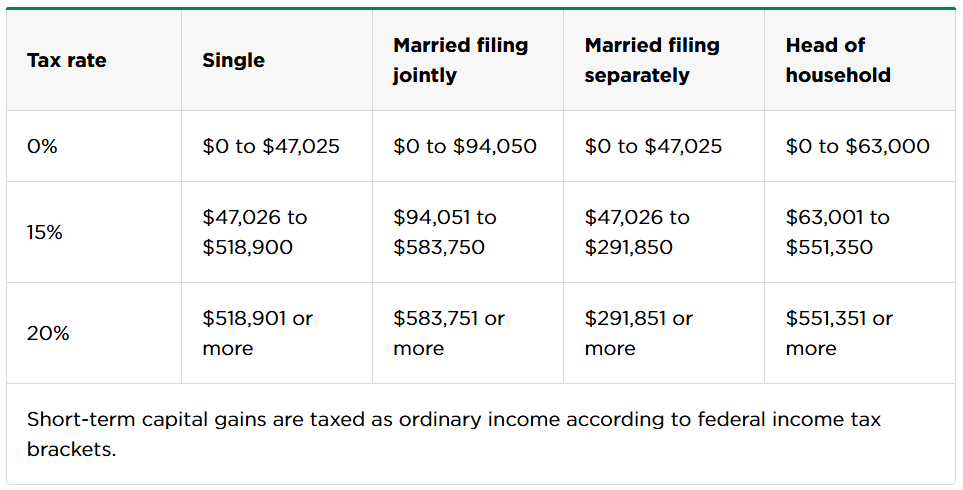

✖️ Investors In Low Tax Brackets

There are 2 kinds of people who might fall into this category: those who have low taxable incomes (from earnings or due to tax savviness) and investors who have held assets long enough to qualify for long term capital gains and qualified dividend rates.

Depending on how much income you’re actually making, or how much your investing income is going to be taxed, it might not be worth it to harvest any losses. Strategy is the key here.

The following chart shows the IRS tax rate on long term capital gains for 2024. This applies to stocks you hold for over a year. Stocks held for a year or less are considered to be short term capital gains and taxed at your standard rate.

Note: Qualified dividends also use this special tax rate chart, but their holding requirements are different. You have to hold a stock for more than 60 days in the 121-day period that began 60 days before the ex-dividend date.

How Does Tax-Loss Harvesting Work

You Need Both Realized Gains And Losses

The IRS doesn’t consider the unrealized gains or losses of your stocks to be usable for tax purposes. You need to sell investments for both gains and losses to be claimed and used.

A gain doesn’t have to occur before a loss. You can do either at any point throughout the tax year and even sell partial positions versus your entire share holdings.

Don’t Trigger The Wash-Sale Rule

When you sell an investment for a loss, you can’t put any money back into the same asset for 30 days.

This includes dividend reinvestments

You need to turn the DRIP off on any stock you sell for a loss to prevent losing your tax deduction. Putting money back into the same or “substantially identical” investment before waiting 30 days will trigger the IRS’s Wash-Sale Rule.

When we sold half of our position in IEP to harvest a tax loss I wasn’t aware that dividend reinvestments were a no-no. Luckily, IEP pays quarterly and the DRIP didn’t reinvest until after the 30 waiting period. Whewww

What Does “Substantially Identical” Mean?

Unfortunately, the IRS doesn’t provide a precise definition of what “substantially identical” securities are. Individual companies are pretty obvious, but it can get confusing when you start looking at funds that hold many different assets.

When I was researching, I saw that in order to comply you can choose replacement securities with similar characteristics but different holdings.

One of the examples I found was that it’s okay to sell a S&P 500 index fund and buy a total market fund.

I’d say when in doubt put it into something that’s obviously not the same thing, wait the 30 days, or consult a professional. Your money doesn’t have to sit idle; there’s always BulletShares.

Which Gains Do You Offset

The IRS requires that your harvested losses must first offset gains of the same type before they can offset other gains. Short-term losses offset short gains. Long-term losses offset long gains.

Short-term applies when you sell a stock in one year or less of buying it. These are taxed at regular ordinary income rates.

Long-term applies when you sell a stock after holding it for more than a year. These are taxed at lower capital gains rates. Most people won’t pay more than 15% on long-term gains.

We already showed you the regular income tax bracket chart and long term capital gain charts in this article. Always use the IRS’s current year’s charts.

Ordinary Income Deductions And Limits

If your losses exceed your gains, you can use up to $3,000 of these losses annually to reduce your ordinary income. If you’re married filing separate, you each get $1,500. This is a pretty sweet gig.

Carryover Losses

If your losses are still higher than the gains you offset and $3,000 deducted from your ordinary income, the remaining unused losses can be carried forward indefinitely to offset future gains.

Note: These were the Federal IRS rules at the time of writing. The tax codes are subject to change in any given year. You’ll have to check your state rules to see if they offer similar tax benefits.

Examples of How Tax Loss Harvesting Would work

When you sell an investment at a loss, the loss can offset capital gains dollar for dollar. For instance, if you have $10,000 in capital gains and realize $7,000 in losses, you’ll only be taxed on $3,000 of gains. The proceeds from the sale can then be reinvested into a similar but not identical security,

Let’s say you made $94,300 from your job and investment income combined. In your taxable brokerage you had realized gains of $10,000 from using our strategy to buy undervalued stocks and sell when they’re overvalued.

Using 2024’s Federal Tax Brackets, you would pay 12% tax on $47,150 ($5,658) and 22% tax on $12,850 ($2,827), resulting in $8,485 total in taxes to be paid. Notice how you’re paying a higher proportion to taxes on money in the higher bracket.

Looking at your portfolio you realize you have $13,000 in losses that you can lock in. This will reduce your taxes down to $5,640. That’s a 33% reduction in your taxes!

Strategy

And if you choose to sell and use the money to invest in the original security again. You’d ultimately be deferring your tax liability rather than reducing it. This might make sense if you’ll have some of your income in a really high tax bracket and want to offset things, but usually it wont.

Just because an investment goes up in price doesn’t mean you should employ tax loss harvesting to balance things out.

Looking over our investing strategy that combines dividend investments and buying undervalued assets and selling when they’ve become overvalued.

We believe this process naturally takes place with our investing strategy and when we are sticking to our allocation strategy.

It makes a lot more sense to turn off your dividend reinvesting DRIP before selling off a position. But we will sell if an asset becomes too overvalued. At that point we can look over our assets and

Schwab has a summary that that shows your short term and long term gains and losses. Which is nice. Don’t know if other brokerage accounts do. Vanguard does not. To see if we should lock in a loss to offset anything. We did this for IEP.

We do not recommend using tax loss harvesting in assets that could rebound fast which often happens in volatile markets. Use extreme caution with yieldmax. I could see a benefit of selling your yieldmax at a loss to offset gains since these have a vastly different structure of being heavy on dividends and not price.

Market and or sector downturns could be a great time to implement this strategy, but if you follow our strategy that’s when we buy. So the only time this seems to be a good strategy is when you have a one off issue like we did with unexpected issues like with IEP unexpected issues like IEP, MPW, or CWH.

If you want to lower your taxable income there are other ways. A big one is to And if you want to make a huge impact to lower this area, consider moving to a state that doesnt tax investment income or doesn’t have state income taxes at all. Examples florida, texas, south dakota.

And if you’re thinking about selling stocks during a pullback just to reduce your taxes, you have a lot more analyzing to do.

Not only does the IRS have a 30 day wait period before you can buy the same stock, but you aren’t actually eliminating taxes. Tax-loss harvesting just defers the gain if you get back into the same stock.

Don’t get me wrong, there could be a time and place for this, but you have to avoid the IRS’s Wash Sale Rule and determine if there’s a risk of losing gains if the stock rebounds while you’re waiting to get back in.

f lost gainsal strategy in the case of there’s also less incentive to risk this when you realize that tax-loss harvesting won’t negate your taxes altogether, it just defers your obligation to pay those gains until later. We’ll talk about why that could be beneficial in the strategy section.

However, we do hold stocks for longer than a year depending on metrics and that can substantially reduce your capital gains taxation. There may be more benefit to holding than selling depending on the situation and math.

Now you could sell for a loss when investments go down and get back in but the IRS has a 30 wait period if you want to get back into a “ substantially identical” security.

There is no incentive for these types of investors as tax loss harvesting won’t negate your taxes altogether, but will defer the gains down the road. You’re better off holding.