If you were hoping for a calm week where inflation politely drifts to 2%, the Fed cuts rates, and everyone holds hands…lol.

We got producer inflation popping again, the weekend turned into a full-blown geopolitical mess, and the labor market is still being stitched together by

healthcare like it’s the only industry left hiring.

Here’s what mattered, what it actually means, and what we’re doing about it.

Economic News

1️⃣ PPI: inflation is still alive and unfortunately thriving

January PPI (producer price index — what companies pay before they pass costs to you) rose 0.5% in January. Year-over-year producer inflation sits at 2.9%.

Now the part that matters: the report shows the “good news” categories (food and energy) fell, while the stuff that actually hits you later is heating up.

- Food: down 1.5% MoM

- Energy: down 2.7% MoM

- Final demand services: up 0.8% (biggest jump since July 2025)

- The monster inside services: trade-service margins jumped 2.5% (aka retailer/wholesaler “we need to cover our costs” margins)

- Core-ish measure (less food/energy/trade services): up 0.3% in January; +3.4% YoY

And yes — some of your “wait WHAT?” sub-components are in the report too, including a 14.4% jump in margins for professional & commercial equipment wholesaling.

Also worth noting: nonferrous metals (in intermediate demand) rose 4.8% MoM.

What it means (in plain English):

Producer-side inflation is pushing up again, and that usually shows up in consumer prices with a lag. This is why rate cuts should be off the table based on inflation data alone.

And the market basically agreed — inflation surprise → rate-cut hopes fade → stocks wobble.

Also yes: BLS notes seasonal factors were recalculated and there were PPI weighting/table changes in this release.

(And separately, I’ll just say it: when you fire people for reporting “bad” data and replace them with loyalists, confidence in the numbers tends to… evaporate.)

Takeaway: This report was not good. And producer inflation has a habit of showing up at your doorstep later with a bill.

2️⃣ “America First” started another conflict

Agent Orange bombed Iran this weekend, and the bombs are still falling. This is not the Venezuela smash-and-grab vibes — this is looking like an actual war scenario.

Markets + war = volatility. Period.

So here’s your reminder, in all caps if needed: DO NOT PANIC SELL.

War headlines can whipsaw prices hard, especially with oil risk and broader risk-off moves.

The Islamic Republic is (understandably) not thrilled their Supreme Leader was killed, and this looks like it could drag.

Takeaway: volatility is the feature, not the bug, during war. If you sell emotionally, you usually sell at the worst possible moment.

3️⃣ ADP: February hiring beat expectations… but it’s basically healthcare doing all the work

Private payrolls for February came in at +63,000, above the expected ~50,000.

But once again the “strength” isn’t broad — it’s concentrated:

- Education & health services: +58,000

- Professional & business services: -30,000

- Manufacturing: -5,000

- Trade/transport/utilities: -1,000

And yes, since the tariff era became a constant nuisance (April 2025), multiple sources estimate manufacturing jobs are down tens of thousands — commonly cited around ~72,000 since that period, depending on the timeframe/source.

Takeaway: the labor market is being held together by healthcare right now. There will come a day when that sector saturates — and then the cracks stop being “cracks.”

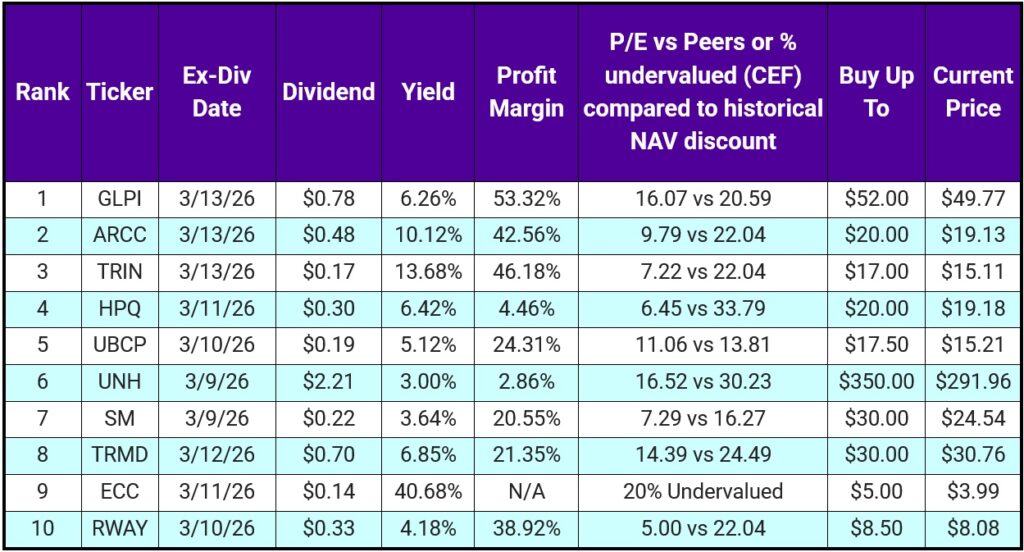

Top 10 IINvestments Going Ex-Dividend Next Week

A lot of names you already know, plus a few “new” ideas. Starting at the bottom:

RWAY

We held it ~9 months. Dividend was cut in 2024 and again in 2025. Payout ratio is high, so I wouldn’t be shocked by another cut in Q3/Q4 2026. Price has trended down since March 2023. I’d expect it to live in the $6.50–$8.50 range for the rest of 2026. “Experts” put fair value around $10.

ECC

Extremely undervalued vs its own history — 20% discount is the low end. They’ve paid $0.14/month since April 2022. The only honest question: how long can a ~40% yield be sustained?

That said: a deep historical discount + even a normal yield gives you cushion. A deep discount + a ridiculous yield is… a lot of cushion if you can stomach the risk.

TRMD

Up 48%+ YTD and you’re not automatically “too late.” I still think it can get above $30 and potentially revisit the $40 area in 2026. But it’s shipping/tankers: dividend is profit-based and can be inconsistent. If you need consistent retirement cash flow, this isn’t your friend.

SM

Formerly CIVI (post-merger). SM looks like a better-run company than CIVI was. Dividend just raised to $0.22 from $0.20 (10%). With merger infrastructure and production scaling (estimates floating around suggest big production and revenue lifts), this one has a real runway. If you’re not in it, at least consider a watchlist slot. Price targets being discussed are roughly $30s (low) to $40s (high).

UNH

Healthcare giant with projected upside in 2026 and a strong dividend growth profile (16-year streak, ~13% 5-year dividend growth). Aging population tailwind. I don’t love paying ~$290, but historically $300 has been the low end of its recent trading range; it’s often sat far higher.

UBCP

Dirt cheap bank stock — roughly ~25% undervalued with a 13-year dividend growth streak and ~10% 5-year dividend growth. Plus it drops specials: this year you’re looking at $0.19 regular + $0.175 special if you’re in by 03/10.

HPQ

No intro needed. Dividend raised 15 straight years, ~10% 5-year dividend growth. Price has still depreciated ~37% over five years, so it’s been a “paid to wait” situation. Targets range $18–$30; with revenue rising the last three years, I lean closer to $25–$27 as a reasonable zone. Collect ~6% while waiting.

TRIN

I’m going to say it again: TRIN just makes you money. 5-year total return around 105%. Revenue +23% YoY (2025), NII +15%, net income +62%. It’s not “just another BDC.” BDCs have been hammered in 2026, so you’re getting TRIN at a discount. We bought at $11 in 2023; $15 is mid-band, and with more strong earnings, $18 isn’t crazy. “Experts” say $20 fair value; I say $18; either way it’s discounted here.

ARCC

Biggest player in the BDC game and (in my view) criminally undervalued (~25%). Dividend growth streak 16 years. Total return ~62% over 5 years. Revenue up ~72% since COVID. Another well-run BDC being punished with the whole sector.

Rule stays: below $20 + we have cash = we buy.

GLPI

Gaming REIT (casinos). Dividend raised every year since COVID. Yield isn’t insane (~6%), but it’s well run. And if you’ve learned anything the last few years: people gamble when they’re depressed. The world is… not exactly cheerful. Projected appreciation ~8% in 2026 + 6% yield = potential ~14% year.

We currently hold: ARCC, TRIN, SM, and TRMD from this list.

Portfolio Updates

1️⃣ Retirement Portfolio

Dividend cash split between DOC (18 shares) and SWKS (5 shares). Both are still undervalued, so we buy.

2️⃣ UAN

We finally hit our sell limit that I placed months ago — we recouped our initial investment by only selling off 22 shares.

This means we have 26 shares of UAN that are all profit. Yes

3️⃣ Vanning Portfolio

Dividend cash (including UAN proceeds) split between:

- NVO (25 shares)

- ARCC (26 shares)

- SBAR (20 shares)

Want Instant Notifications For These Investing IINsights?

We post these updates to several places where you can subscribe and get notified as soon as we post.

- Substack

- LinkedIn Newsletter

- Our email list (no spam, just 1 email a week). Sign up below.