I love tacos. Breakfast tacos, street tacos, weird homemade tacos — all of it.

But I finally found a taco I don’t care for: the taco trade.

Because when the market becomes a giant emotional yo-yo based on one man’s mood swings, it stops being investing and turns into group therapy with charts.

Anyways. On to the actual data, then the ex-div list, and our portfolio updates.

Economic News

1️⃣ Jobs report: bounce back… but the foundation is still yucky

The latest jobs report dropped today. In March the economy added 178,000 jobs, which was awesome considering February’s revised numbers had the economy losing 133,000 jobs.

But again — look at where the jobs were added:

- Health care: +76,000

- Construction: +26,000

- Transportation & warehouse: +21,000

Big losers in March:

- Government: –18,000

- Financial activities: –15,000

- Manufacturing: –6,000 (and down 80,000+ jobs YTD)

Now, I do see some fudging in the numbers because a narrative is being pushed:

“The labor market is fine outside government employees — the weak job numbers are just government trimming.”

This is horseshit. The trimming happened last year with DOGE.

The labor market is teetering and the “official” numbers the last few months show it:

- January: +160,000

- February: -133,000

- March: +178,000

And if we go back further:

- October: -173,000

- November: +56,000

- December: +50,000

That’s a pattern. The “good” months are weak. The “bad” months are ugly. And when you combine the last six months, you get 138,000 jobs added total — about 23,000 per month.

And remember: these are Agent Orange and his minions’ own numbers. He fired the head of jobs numbers and replaced them with a loyalist.

23,000 jobs a month is trashpanda. Worst stretch since 2003.

For comparison:

- “Sleepy Joe” averaged 380,000 jobs/month in 2022

- 251,000 jobs/month in 2023

- 168,000 jobs/month in 2024

Agent Orange’s own doctored numbers show 23,000.

Enough said.

2️⃣ The taco trade and why I hate it

If you’re not familiar: TACO stands for “Trump Always Chickens Out.” And yes, people have made boatloads of money on it.

It goes like this:

- Agent Orange makes a threat

- Markets tank because the demand is bat shit crazy

- Everyone knows the Orange Horsie will backtrack when markets tank

- People buy the dip

- He “chickens out”

- Markets rip higher

- Rinse, repeat

The “not a war” war in Iran is another instance of the Taco Truck Trade.

This week, on Easter, Agent Orange made some batshit demands and mentioned blowing up the entire country. Markets tanked, people bought the dip, and now we have a two-week ceasefire. Markets exploded higher.

I’m sure this drags on longer. And in two weeks the Orange Horsie will say some dumb shit, markets will tank, rinse, repeat.

The reason I don’t care for Taco Truck Trades is simple: it has nothing to do with market health or financials. It’s pure momentum and sentiment — emotional trading that defies logic.

Sadly… to be continued.

3️⃣ PCE 3% YoY + consumer spending down + GDP revised down again

As none of you should be surprised (we’ve discussed it repeatedly), the February PCE inflation rate came in at 3% YoY.

But the more troubling stuff dropped at the same time:

- Consumer spending decreased 0.1% in February

- Q4 GDP revised down to 0.5% (from 0.7%, from 1.4%)

I hope you’re starting to see the pattern with economic data recently:

A number is presented that’s “fine” — GDP at 1.4%, jobs created at 130,000, etc.

The regime knows markets won’t tank on average/slightly below average numbers.

Then over the next couple months, those numbers get revised down. 1.4% to 0.5% GDP in two months is cra-cra. Same with jobs getting revised down from “fine” to “actually weak.”

This is being done strategically to keep everyone invested.

Back to inflation: 3.0% should send shock waves through the market, but it won’t — because everyone is swooning over a shiny new “ceasefire.”

And 3.0% inflation before the shitshow that is $115 oil means inflation could post obscene numbers in a couple months.

Consumers know it. They’re tightening the belt. That’s why the “experts” projected +0.6% consumer spending in February and the actual number was -0.1%.

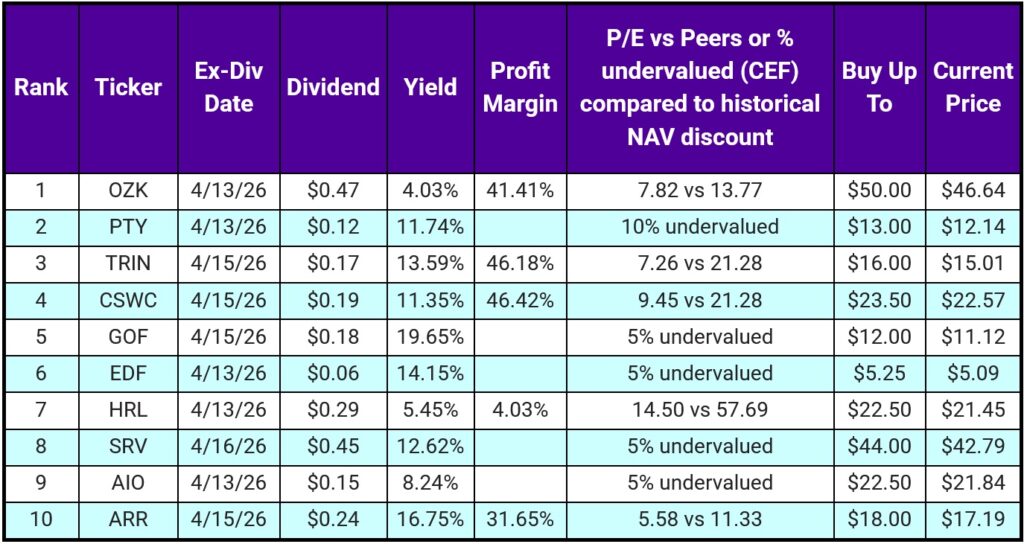

Top 10 IINvestments Going Ex-Dividend Next Week

As usual the past few weeks: markets are volatile as shit and prices are all over the place. Make sure prices are reasonable when placing an order.

We have five CEFs this week. I know that’s a lot, but these are actually very good deals after the recent selloff and volatility.

PTY

PTY gives you a ~12% yield on a CEF that almost always trades at a premium. Over the 24 years since inception, it averages about a 14% premium. Recently you could buy it at only a 6% premium.

Why? Because the market treated anything tied to private credit like it was the same as banks limiting withdrawals. Sell first, ask questions later.

That panic is a buying opportunity. I’m really high on PTY here:

- at minimum 8% undervalued (relative to its normal premium)

- plus ~12% yield

- very real chance at 15%–20% total return over the next 12 months on a ~$12 CEF.

GOF

GOF gives you a slap-your-own-ass 20% yield and a similar setup.

Over 19 years since inception it mostly traded at a premium; average premium around 9%. Right now it’s around a 3% premium → about 6% undervalued relative to normal.

It has exposure to below investment grade bonds, and with the world in panic mode, you know how it goes: sell, sell, sell.

I’m also high on GOF for the next 12 months:

- potential for 20%–25% total return on an $11 CEF is on the table.

EDF

Emerging markets CEF with the same setup. Historically trades around a 7% premium (since inception ~16 years ago). Right now it’s about a 4% premium.

3% doesn’t sound like much, but this is a $5 CEF yielding 14%. That’s where the monster gain potential comes from.

Emerging markets have been crushing it, so why is EDF “undervalued”? I can’t find anything in the news or portfolio that makes me worry. It looks like it got sold off with everything else.

SRV

Another head scratcher: with oil exploding, somehow SRV is 5% undervalued. No clue why.

SRV is our play for holding a bunch of energy names in one CEF that yields 12.5%.

Best part: no K-1s. Yay.

AIO

I do know why AIO is undervalued: AI has been getting killed in 2026. Is it warranted? No. Buying opportunity.

AIO holds strong tech names, yields 8%+, and it’s undervalued. Yay.

Bottom line: all five of these CEFs have a high probability of generating 10%+ total return over the next 12 months, and a couple could be closer to 20%.

Now on to the five stocks.

ARR

mREIT with a super high yield. Recent cash flow covered it, but the risk is the mortgage spread.

ARR borrows to buy mortgages. If the borrowing cost climbs or spreads compress, the cash flow that supports the yield evaporates.

High risk, super high reward.

HRL

59-year dividend growth streak, 5-year DGR around 4%.

Now the ugly:

- gross margins down 5%–10% YoY

- net margins down 30%–40% YoY

- revenue and EPS down around 40%

Why? Three big reasons:

- Tariffs + input costs: pork +30%, beef +20%, turkey +40% (plus avian flu), which eroded profits

- HRL can’t pass those costs on without losing customers → tons of competition

- Ozempic/GLP-1 effect: people eating less. Ozempic users spend 11% less on food per year. If 12%–13% of adults are using GLP-1s, that’s a lot of cheese off grocery bills.

All of that needs to stabilize before I’d be super confident holding HRL.

CSWC

BDC. Three-year dividend growth streak, but the real question is coverage.

Last earnings:

- NII $0.60

- regular dividend: $0.19/month → ~95% payout for the regular dividend

CSWC usually pays $0.06/quarter in specials (not covered by NII), but it has 17 quarters of spillover cash, so I’m not worried about the dividend right now.

My concern is floating-rate loans. People smarter than me estimate every 1% of rate cuts reduces NII by $0.23–$0.24/share. If rates get cut, coverage gets tighter.

TRIN

My favorite BDC. Money-printing BDC.

Latest:

- NII $0.52 barely covers the $0.17/month dividend → 98% payout

- only 5 months of spillover cash (not a ton of cushion)

- non-accruals 1% (amazing; typical is 3.8%–4%)

TRIN also has many loans at/near rate floors. Normally I don’t care, but clearly whatever they’re doing works: even after 0.75% rate cuts, NII was a record $2.08 in 2025.

TRIN usually trades in a $14–$16 band. Under $15? High probability you make money. I expect 17%–20% total return in the next 12 months.

OZK

OZK has a 30-year dividend growth streak, 5-year dividend growth around 10.5% (BANANAS).

Payout ratio 29%, and the streak of 63 consecutive quarters of dividend raises should continue. Yes, they’ve raised the dividend every quarter for over 15 years. Like I said: BANANAS.

ROE 12% in 2025, record EPS $6.18 in 2025, and I’m pretty sure it’s 10%+ undervalued.

No brainer: buy OZK anytime it’s below $46.

Portfolio Updates

1️⃣ Retirement portfolio: Bought STWD

Cash in the retirement portfolio was used to pick up 26 shares of STWD.

STWD is 20%–40% undervalued depending on source. I have it at the low end, around 21% undervalued.

Projections for this 11% yielding mREIT are off the mofo chains:

- revenue projected from $548M (2025) to $2.1B (2026)

- revenue projected to grow 39.3% per year next five years

- EPS projected up 60% from 2025 to 2026, then 9.3%/yr next five years

- management allocating 6% total share buyback (company thinks the stock is deeply discounted)

There’s a lot to like, so we’ll keep buying dips.

2️⃣ Vanning portfolio: THTA + SBAR

Cash in the vanning portfolio went into:

- THTA (3 shares)

- SBAR (5 shares)

I’m waiting on a couple potential pickups to settle a little before deploying more.

Want Instant Notifications For These Investing IINsights?

We post these updates to several places where you can subscribe and get notified as soon as we post.

- Substack

- LinkedIn Newsletter

- Our email list (no spam, just 1 email a week). Sign up below.