If you’ve been feeling like we’re playing economic Jenga—pulling pieces out and pretending the tower is “fine”—this week didn’t exactly calm that down.

We got slower growth, hotter inflation, and then the Supreme Court tossed a legal grenade into the whole tariff situation. So yeah. Another normal week.

Here’s what mattered, what it likely means, and what we did in the portfolios.

Economic News

1️⃣ GDP: Slower than advertised

Q4 GDP grew at 1.4%, which is much lower than the projected ~2.9%. Full-year GDP for 2025 came in at 2.2%, down from 2.8% in 2024.

The most telling nugget for me wasn’t the headline—it was the mix:

- Spending on services: up 3.4% vs Q3

- Spending on goods: down 0.1%

Translation: we’re paying more for stuff, so we’re buying less stuff and shifting toward services. That’s not “consumer strength.” That’s consumer triage.

Takeaway: growth is slowing, and the consumer is making “keep the lights on” decisions.

2️⃣ PCE inflation: still not behaving

We also got December inflation data, and it was hot again.

- PCE price index: up 0.4% MoM

- Year-over-year PCE: 2.9%

- Core PCE YoY: 3.0%

So whether you want to call it “3%” or “basically 3%,” the point is the same: inflation is not politely returning to target.

Takeaway: we’ve got slower growth + sticky inflation. That’s the kind of combo that eventually forces something to break (policy, earnings, credit, employment… pick your poison).

3️⃣ Supreme Court + tariffs: welcome to the chaos phase

The Supreme Court just ruled the President does not have the power to issue tariffs under the provision Agent Orange used (IEEPA).

This is where it gets bonkers:

- If tariffs imposed under that authority are invalid, you’re immediately talking about legal fights, compliance whiplash, and potential refund/repayment questions (depending on how implementation and litigation shake out).

- If the tariffs truly come off (or are materially reduced), it’s possible you get a growth bump and inflation relief… because you’ve removed what functionally acted like a consumer tax.

This story is far from over. I’m sure Agent Orange will have something to say and do about this.

Takeaway: the tariff “tax” just got challenged at the highest level, and markets hate uncertainty almost as much as they hate earnings misses.

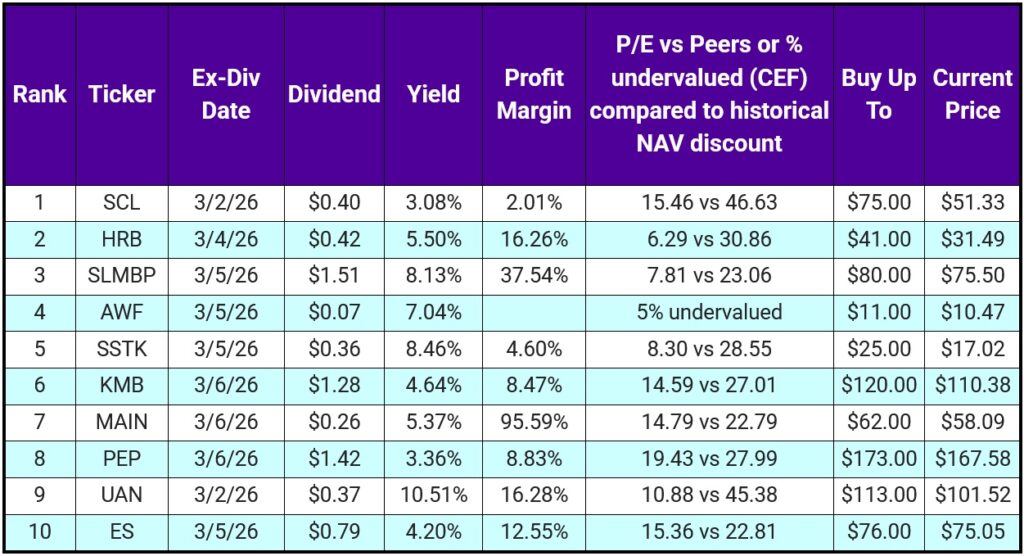

Top 10 IINvestments Going Ex-Dividend Next Week

This week’s list is banging—not because the yields scream at you, but because the quality underneath is strong.

You’ve got: 6 dividend growers, a preferred that’s deeply discounted, a bond CEF with room to run, a wild fertilizer payer, and one of the best monthly-pay BDCs out there.

Here’s the rundown.

SCL

58-year dividend growth streak. Yield ~3% doesn’t look flashy, but the 5-year dividend growth rate is ~6.6%/yr. Chemical sector = bumpy ride, but you get paid to wait while value catches up.

HRB

8-year dividend growth streak. It’s tax season. HRB is one of the main places people go when their taxes get complicated (or when they’d rather pay someone than cry into a spreadsheet). Mad undervalued, and the 5-year dividend growth is ~9%/yr.

SLMBP

Preferred for SLM. Par is $100, currently discounted hard, and the yield is absurd. (Preferreds are their own animal—know what you own, but yes: the math is attractive here.)

AWF

Closed-end bond fund trading about 5% below its historical discount. Established 1993, so the historical discount data actually matters. This one has legs.

SSTK

6-year dividend growth streak. Mergers in the works, which can help or hurt share price. It’s Shutterstock—the “picture thing you see everywhere on the internet.”

KMB

53-year dividend growth streak. 5-year dividend growth (~3.3%/yr) isn’t as spicy as SCL/HRB, but KMB is everywhere (Kleenex, Huggies, Kotex, Scott, etc.). Staple for an income portfolio.

MAIN

We talk about MAIN a lot for a reason: remarkable financials, strong dividend, well-run. Only issue is price.

My rule stays the same:

- Above $62 = overvalued → DRIP off

- Back to $56–$58 = DRIP on

Rinse and repeat if you want to maximize yield efficiency.

PEP

Pepsi—no intro needed. 54 straight years of dividend increases. 5-year dividend growth ~6.8%. The only real debate is price. Depending on source, target range is $150–$198; in our equation fair value is $173.

UAN

The wildest ride you’ll ever experience with a boring fertilizer stock. Price swings are violent. Dividend is variable (one quarter $0.40, another quarter $2+).

Fair value: $113 in our work. Do not overpay. If you wait a week or two, odds are you can get it under $100. (We got it at $82 in 2023. Still proud of that one.)

ES

Utility with a 26-year dividend growth streak and ~5.8% 5-year growth rate. Boring… in a good way.

Price rule:

- Above $80 = overvalued → DRIP off

- $74–$75 or less = DRIP on

Portfolio Updates

1️⃣ New position: TROW

We sold some dry powder (THTA & SBAR) to initiate a new position in the vanning portfolio: TROW.

Why now:

- 39-year dividend growth streak

- 13.6% projected growth each of the next 5 years

- Trading about 30% below fair value (in our work)

- We bought 53 shares

Earnings on 02/04/2026 were mixed and the stock has been volatile, but I think the worst is behind it.

Forward-looking numbers:

- EPS projected up ~14% in 2026

- Revenue projected up ~8% in 2026

- P/E, P/S, and P/B at 5-year lows vs its own history

- Total shareholder return (price + dividends + buybacks) has risen from 3.67% (2021) to about 7% now

The fun part: not one expert has it as a buy, which is exactly how we like it. Getting in before the masses.

Warnings:

- ~10% short interest, so volatility stays elevated short-term.

Price targets:

- 12-month: $116–$130 (about 23%–38% upside from here)

- 5-year: $152–$175 (about 62%–86% upside)

Dividend:

- ~5.5% yield, just raised 2.5% to $1.30/share.

Cha-ching.

2️⃣ New position: NVO

Another one I’ve been watching is in pharma. We already have BMY, but didn’t get as much as I wanted before it ran.

The one I’ve been waiting for: NVO.

It’s down ~20% YTD and just tanked because its weight loss drug performed 2% lower than its competition in a long trial. That is… exactly the kind of overreaction we like to buy into.

Why I like it:

- Dividend growth streak 29 years (per Sure Dividend)

- Projected EPS growth 8%+ per year next 5 years

- Profitability metrics are obscene: ROE 60.70%, ROIC 41.13%, ROCE 43.00%, ROA 17.43%

(Translation: they know how to make money.)

We initiated 50 shares in the vanning portfolio.

Yes, yield tradeoff:

- THTA yields 12% and pays monthly

- NVO yields about 4% right now (and pays 1–2x/year depending on FCF), with a typical 5-year yield range of ~1.4%–1.9%

So we’re getting paid meaningfully more than its historical yield while we wait.

Valuation / upside:

- Fair value estimates: $55 to $70 depending on source

- 5-year projected price: $101

That implies NVO is ~37% undervalued (low end) to ~75% undervalued (high end), with projected 5-year price growth around 153%.

If those numbers hold, you’re looking at a projected CAGR around 18.7%–19.9%.

Risk note: pharma is volatile by nature. If your risk appetite is limited, pharma stocks may not be for you.

3️⃣ Watchlist update (2026)

We’ve moved BDX, MKC, and NNN onto the watchlist for the remainder of 2026. Would not be shocked to initiate one or more positions later this year.

4️⃣ Retirement portfolio: added dry powder

Cash this week went into more dry powder: 10 shares of THTA.

5️⃣ CWH: the dividend pause

CWH paused the dividend—even with ~$215M cash on hand and debt reduced almost in half. Shares tanked after earnings, as they should.

We’re already down enough that throwing a few hundred more at it isn’t a big deal for us, but if you’re holding CWH: sell it and redeploy into something that actually pays you. Income is the point.

6️⃣ LYB: dividend cut

LYB cut the dividend in half until the chemical environment improves. If you hold it, you’ve got a decision to make.

By earnings/projections, LYB is still about 15%–25% undervalued, but yield is now ~6% instead of 12%.

We’re holding because we’re up ~20%. Once price gets above $60, we’ll start taking profits until our initial investment is recouped.

Want Instant Notifications For These Investing IINsights?

We post these updates to several places where you can subscribe and get notified as soon as we post.

- Substack

- LinkedIn Newsletter

- Our email list (no spam, just 1 email a week). Sign up below.