If you thought last week’s economic circus was wild, this week said “hold my beer.” Between manipulated jobs data, Fed linguistic gymnastics, and a shiny new ETF that pays twice a week, there’s plenty to unpack. Let’s cut through the noise, talk about what actually matters, and look at how we’re moving money inside the portfolios.

Economic News

1️⃣ Consumer Sentiment Dips Again

September sentiment dropped 4.8% from August, with three big sore spots:

- Personal finances down 8%

- Tariffs up as a concern (+4.3%)

- Inflation expectations climbing (4.8% within 12 months; 5-year outlook now 3.9% vs. 3.5% in August)

This isn’t perfect data, but it’s a peek into how actual people feel. And right now, they’re worried—about bills, prices, and whether tariffs are strangling their financial journey.

2️⃣ Retail Sales = “Feels Good, But…”

Retail sales rose 0.6% MoM and 5.0% YoY in August. That looks strong—until you account for inflation. Adjusted, it’s closer to 0.2% MoM and 2.0% YoY.

Consumers are still spending on new cars, online shopping, and restaurants—things you don’t do if you fear losing your job. But here’s the contradiction: people feel broke (see sentiment above) while spending like they’re flush.

3️⃣ The Fed Finally Cuts

The “worst-kept secret” became official: a 0.25% rate cut. What made Wall Street salivate was the Fed hinting at two more cuts in 2025, bringing rates down 0.75% by 2026.

The excuse? A softening labor market. Translation: the Fed chose jobs over inflation. Expect ~3% inflation to stick around. On the flip side: BDCs and REITs should shine over the next 6–12 months. Our portfolios are already set up for this environment.

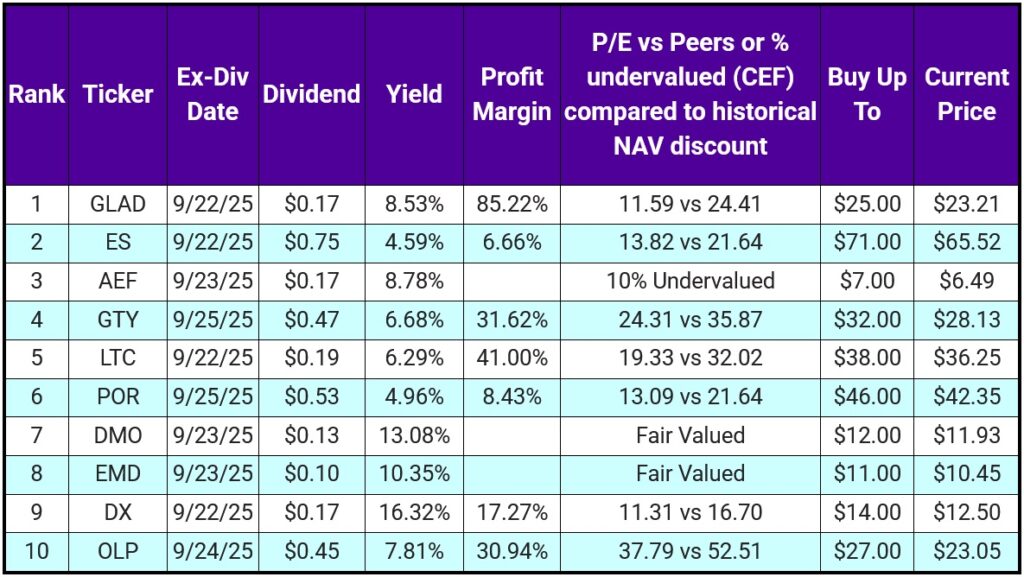

Top 10 IINvestments Going Ex-Dividend Next Week

Not a fireworks show, but there’s solid meat here:

- 3 CEFs: AEF, DMO, EMD

- 3 REITs: GTY, LTC, OLP

- 2 Electric Utilities: ES, POR

- 1 BDC: GLAD

- 1 mREIT: DX

👉 Standouts:

- AEF (see Portfolio Update): Long-term potential, undervalued, 8% yield.

- DX: Juicy yield, but high-risk.

- OLP: Diversified REIT with a broad property bag.

We currently hold ES and LTC, and have previously owned GLAD, EMD, and DX.

Portfolio Updates

1️⃣ Goodbye (Mostly) SBLK – Death by Weak Dividends

We finally pulled the trigger on Star Bulk Carriers (SBLK), selling $3,000 worth and keeping about $1,900 on the side. Why? Dividends. Or rather, the lack thereof. To date in 2025, SBLK has paid a laughable $0.19/share total across 3 payouts. That’s barely 6 cents a quarter—completely unacceptable for what was supposed to be a reliable income play.

Thought process: Shipping is volatile, and while coal/energy demand could give SBLK a bump later, we can’t have dead weight clogging a dividend portfolio. We held back a smaller chunk as a lottery ticket in case dividends rebound, but we’re not tying up real capital in hope-and-pray mode.

2️⃣ TGT, LTC & CMG – Recycling Capital Into Winners

The proceeds from SBLK went into Target (TGT), LTC Properties (LTC), and Chipotle (CMG).

- TGT: Trading under $100, this is a textbook undervaluation play. 54 years of dividend increases (a Dividend King), and while the “woke ad” backlash dinged traffic, the fundamentals are improving. We’re building this position as long as it stays cheap.

- LTC: Aging boomers = 10,000 retirements per day. Healthcare REIT exposure is a must, and LTC’s ~6.5% yield plus revenue growth made it the clear add. It’s also monthly-paying, which smooths out portfolio income.

- CMG: The outlier. Doesn’t pay a dividend, but sometimes growth is worth it. With margins expanding and same-store sales rising, CMG adds a splash of capital appreciation to balance the high-yield plays.

3️⃣ INTC – The Call That Paid Off

We’ve been pounding the table on Intel (INTC) since 08/2024 (and again in 01/2025), and the payoff has been massive:

- U.S. Government: Bought a 10% stake (rare endorsement).

- SoftBank: Dropped $2B.

- NVIDIA: Just invested $5B to partner on data centers and chip manufacturing.

This is what happens when you buy during the dark times. INTC looked ugly a year ago, but our thesis was simple: undervalued, too critical to fail, and too much future demand for chips to stay sidelined. If you followed our lead, congrats—you made ass amounts of money on this one.

4️⃣ AEF – New Emerging Market Exposure (Ex-China)

In the retirement portfolio, we initiated a position in Aberdeen Emerging Markets Fund (AEF). Why this one?

- About 10% undervalued right now.

- Pays ~8% yield.

- Excludes China, which reduces political volatility while still capturing emerging market growth.

- Founded in 1989, so it’s survived multiple financial crises and kept paying.

Yes, it’s trading near a 52-week high, but with fundamentals this solid, we’d rather get in now ahead of the 9/23 ex-div date and collect right away.

5️⃣ QLDY – A New Type of Payer on Watch

Not in the portfolio (yet), but worth mentioning: QLDY just launched as the first ETF to pay dividends twice a week. We’re not piling in blind, but this could be a game-changer for people running income-focused portfolios. We’ll watch the data before committing.

Want Instant Notifications For These Investing IINsights?

We post these updates to several places where you can subscribe and get notified as soon as we post.

- Substack

- LinkedIn Newsletter

- Our email list (no spam, just 1 email a week). Sign up below.