Not much sugarcoating this week. Macro is messy, volatility is the point, and the “this will be quick” narrative is aging like milk.

So we’re doing what we always do in weeks like this: stay disciplined, stay income-focused, and use chaos to reposition instead of panic-selling into it.

Economic News

1️⃣ A Short “War Not War”, Yeah Sure

We’re now three weeks into a “not a war” war that Agent Orange told us would last “only a few days.”

The Strait of Hormuz is still closed, and prices on oil, sulfur, helium, fertilizer and other inputs are still climbing like they’re training for a marathon.

With no end in sight, you’re starting to see the word “recession” leak into mainstream media again. And if oil hits and stays in the $160–$180 per barrel range? The odds of a global recession go from “possible” to more likely so authority sentiment should probably stop pretending everything is fine.

Could this “not a war” war tank your portfolio? Yep. Pretty bad. Even ours is down $11k so far. But here’s the thing, this is now the fourth shock to markets since 2019.

Covid, Inflation, and Tariffs didn’t brake the markets, so I highly doubt stupid wars will either.

Stay strong, my friends.

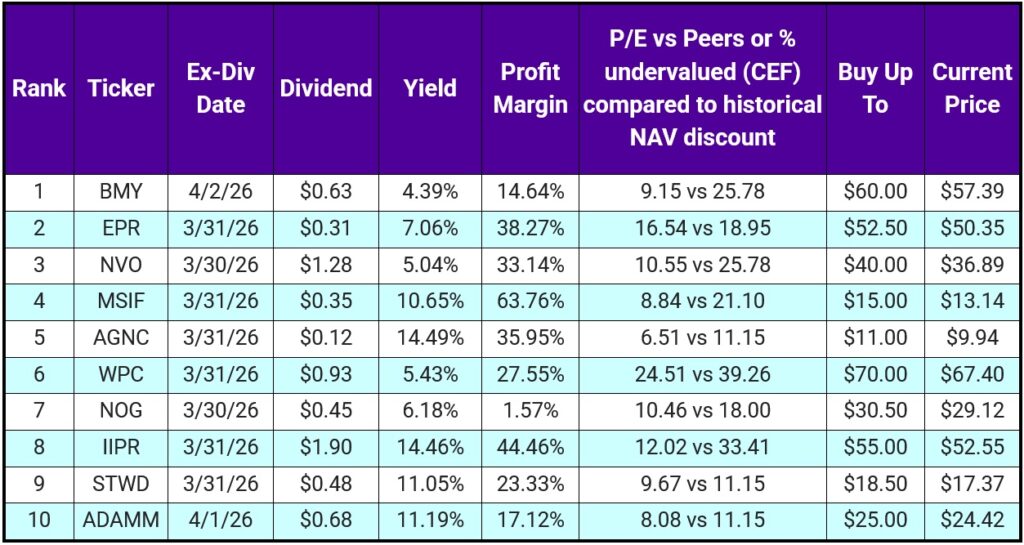

Top 10 IINvestments Going Ex-Dividend Next Week

Preface: Check prices before doing anything. This list was completed on 03/25 and markets have been uber volatile. Verify before you buy.

Truth be told, it was hard to get this list down to 10 from 20 this week. There were like three other mREITs and four other BDCs that didn’t make the cut. So… yeah. It’s one of those weeks.

Starting at the bottom:

ADAMM / STWD / AGNC (the mREIT trio)

ADAMM is a preferred stock for ADAM, a smaller mREIT that has all the metrics of a stock that should rebound once rate talk is less about market volatility/private credit panic and more about, you know… actual interest rates. Smaller company = more robust growth potential because of its portfolio mix (residential, agency, business loans).

STWD is the more “stable” mREIT in this group, with a portfolio heavy on commercial loans plus direct real estate ownership.

AGNC is the high-leverage, low-credit-risk machine: monthly dividend funded off government-backed securities.

We hold AGNC and STWD.

- If you want cash flow, you want AGNC.

- If you want total return + peace of mind, you want STWD.

- If you want a set-it-and-forget-it route, ADAMM is probably the lane.

IIPR

We’ve talked about IIPR a lot over the years. It’s basically the landlord for a ton of CBD/dispensary-related real estate you see popping up.

It has grown its dividend for 8 consecutive years, but if tenant trouble continues, a cut could be warranted. Last earnings:

- AFFO: $1.88

- Dividend: $1.90

So… yeah. That’s tight.

Revenue declined 13% YoY, and there were new tenant defaults. If you’re buying IIPR, you need to research the tenant situation and accept that a dividend cut is on the table.

IIPR does have a boatload of cash, so it can survive bad quarters. My data says it’s fair valued here. “Experts” say $57 is fair value. Either way, with a 14%–15% dividend cushion, you can still get a decent total return even if price pulls back.

NOG

Oil and gas name trading toward the top of its 52-week range.

Dividend has been raised 4 consecutive years and revenue grew 11% YoY even with oil prices being lower in 2025. Production was 6% higher YoY, and the rest of the metrics don’t exactly scream “this should trade like a dumpster.”

6% yield with potential appreciation toward $33, with predicted growth of 12% per year for the next 5 years.

WPC

WPC is somewhat like STWD in that it has real assets plus portfolio exposure, but the structure matters: WPC finances deals by issuing shares.

That’s obvious in the share count:

- ~187M shares five years ago

- ~222M shares today

That high share count is likely part of why the dividend was cut two years ago (it had a 24-year streak before the cut). Good news: management has raised the dividend 8 times since the cut.

So you’ve got a well-run company projected to grow revenue ~3% per year over the next five years, offering a rapidly growing ~5% yield.

FFO is projected at $5.18/share this year, dividend sits at $3.72/share.

MSIF

MSIF is a newer BDC under the same management umbrella that brings you MAIN. Unlike MAIN, MSIF invests primarily in private loans.

Key points:

- trading at 0.83x price-to-NAV (anything under 1 means you’re buying assets at a discount)

- NAV per share now $15.85, up from $14.56 in 2020 (about ~2% NAV growth per year)

- NII grew from $53.9M (2024) to $61.8M (2025) (a 14.7% increase)

My data suggests MSIF is 15%–19% undervalued right now.

NVO

NVO has a 29-year dividend growth streak.

Projections suggest 8% YoY earnings growth for the next 5 years (about 18.7% total return) and a current discount of 31% to fair value.

Latest earnings snapshot:

- Sales up 6% YoY

- Earnings up 2% YoY

- Payout ratio around 50% → dividend streak should be fine

And buybacks matter here:

- NVO has been buying back shares since 2024

- already removed 32.65M shares

- projections for an additional 206M shares bought back by 2031

Less shares = higher prices for existing shares and more dividend increases.

That’s the game.

EPR

EPR is the entertainment REIT with a 5-year dividend growth streak.

AFFO covers the dividend easily:

- $5.35 AFFO

- $3.72 dividend

Revenue up 3.2% YoY, rental revenue up $8M YoY. Projections are ~5% earnings growth and 12% total return YoY for the next five years.

Nobody talks about this company, but it’s a well-run machine. Price targets around $59, which puts it roughly 19% undervalued at current price.

BMY

BMY has a 19-year dividend growth streak and has bought back about 250M shares in the past 5 years.

Revenue growth has been real:

- $26.1B (2020) → $48.2B (2025)

I named BMY one of my 5 stocks to own for the next decade for a reason: pipeline + growth portfolio + international growth.

International growth was 7% in 2025. The “Growth Portfolio” (Opdivo, Reblozyl, Camzyos, Breyanzi, etc.) is now roughly 60% of revenue and growing at double-digit rates.

Analysts are watching Cobenfy (formerly KarXT), approved late 2024, with expectations it can reach $2.6B in sales by 2030. And 2026 is pivotal with 6–7 registrational trial readouts expected, including Milvexian (cardio) and Iberdomide (multiple myeloma).

I have BMY undervalued by around 35%, and you get a 4.4% yield while you wait for price to catch up.

Portfolio Updates

1️⃣ We sold YMAX

One of our longest-held income ETFs dropped its dividend by $0.03 this week. I said “no thanks” and sold YMAX right away.

We’ve held YMAX since April 2024—about 2 years. And while everyone screams “avoid YieldMax, you can’t make money in those ETFs,” we pulled a 25% total return.

Here’s the reality:

- Bought 04/2024 at $18.65/share

- Sold today at $8.00/share

If we had DRIP’d, we would’ve been totally and royally screwed.

But we didn’t. We took the cash and lowered our cost basis weekly.

Here are the numbers:

- Initial purchase amount: $4,089

- Cash dividends collected: $3,072

- Final sale amount: $2,023

Every now and then I do know what I’m talking about.

Rule: If you DRIP high-yield ETFs, the probability is off-the-charts bad that you will lose.

If you take the cash and move it into better investments, you can beat the high-yield ETF trap.

2️⃣ With YMAX proceeds

In the income portfolio, we’re putting:

- $1,000 into XDTE

- $1,000 into QDTE

I want to test these zero-day options ETFs from Roundhill and see what’s what. I suspect we may take a hit in overall monthly cash, but I am 100% certain a reverse split was coming for YMAX and I wanted to avoid that at all costs.

3️⃣ Bought More DOC

Cash in the retirement portfolio went into DOC (10 shares) this week, even though I had other temptations (OZK, DX, KMB, etc.).

4️⃣ Invested In 2 New ETFs

Two new additions. Both riskier. Both absolutely my cup of tea.

First: MINY (50 shares)

Yes, I know—another YieldMax ETF. But unlike 90% of the synthetic call ETFs, MINY is covered calls on stocks in the mining/precious metals sector.

I’m a huge proponent of rare earth minerals in 2026 and 2027 so the U.S. can narrow the gap with China and Russia. The U.S. government is taking stakes in rare earth companies for that exact reason. Some (not all) of MINY’s holdings relate to rare earths.

Upside is likely capped. That’s fine. This is a macrotrend weekly income play.

Second: GIF (162 shares)

GIF is a Rex Shares ETF (I REALLY like Rex Shares). It writes covered calls on 50% of holdings, and the other 50% is structured so the ETF can still realize upside (with slight leverage). It’s like YMAX or WPAY, but with a better twist.

Rex holds names like PLTR, WMT, LLY, TSLA, COIN and:

- writes options on half

- lets the other half move with the market

- pays weekly

Basically: I want more cash for the main portfolio. After a couple weeks/months, DRIP will be off on both—same as AIPI and FEPI. I’ll toggle DRIP on/off based on valuations.

To fund MINY and GIF, we sold 244 shares of SBAR (about $61/month in dividends).

But MINY + GIF should generate around $25–$30 weekly, meaning we went from $61/month to roughly $100–$120/month.

Want Instant Notifications For These Investing IINsights?

We post these updates to several places where you can subscribe and get notified as soon as we post.

- Substack

- LinkedIn Newsletter

- Our email list (no spam, just 1 email a week). Sign up below.