Welcome back to another round of “economic data roulette,” where the numbers spin, the regime shrugs, and we try to make sense of the mess while still building income. This week we finally got the long-delayed September reports (thanks, shutdown), and—shocker—none of it matches the headlines we were fed at the time.

Manufacturing? Flat.

Jobs? Ugly.

Tariffs? Doing exactly the opposite of what we were promised.

But don’t worry, dividends are still showing up on time, the ex-dividend list is weirdly strong, and we made a couple of strategic additions to both portfolios.

Let’s dive in.

Economic News

1️⃣ Manufacturing: Still Waiting on That Tariff “Boom”…

Remember back in April—back when gas was cheaper, inflation was definitely “transitory,” and we were told tariffs would heroically bring manufacturing roaring back to America?

Well, the long-delayed September manufacturing report finally dropped. Brace yourself:

- September increased… 0.0%.

- Flat. Exactly like August’s stunning +0.1%.

Why?

Because tariffs are restricting imports so severely that the entire manufacturing chain is getting squeezed — by the administration’s own data.

YoY manufacturing is up 1.5%, and Q3 2025 was 1.3% higher than Q3 2024, which would sound great if Q2 hadn’t been up 2.4% YoY.

Translation:

We were supposed to be in a tariff-powered boom.

Instead we’re producing 1.1% less than before tariffs kicked in.

Winning.

2️⃣ ADP Jobs Report: Small Business Just Got Body-Slammed

Remember September’s BLS report claiming a magical +119,000 jobs added? Remember how good that sounded—if you ignored the ADP private data screaming the opposite?

November’s ADP update just landed and… yeah. It’s bad.

- Total private jobs: –32,000

- Companies with 50+ employees: +90,000 jobs

- Small businesses (<50 employees): –120,000 jobs

So the backbone of America is losing jobs so fast that the headline number couldn’t hide it.

This is also the last employment data before the next Fed meeting.

Should be a fun week. Grab popcorn.

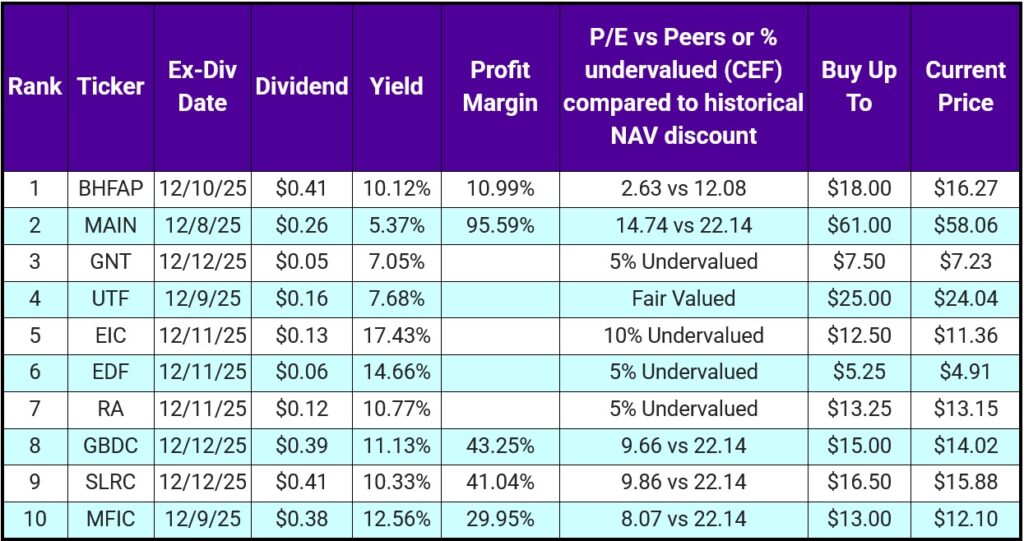

Top 10 IINvestments Going Ex-Dividend Next Week

At first glance this list looks like it has the diversification of a ham sandwich—4 BDCs and 5 CEFs. But look closer…

The 5 CEFs cover completely different sectors:

- GNT – gold & natural resources

- UTF – infrastructure

- EIC – high-yield bonds

- EDF – emerging markets

- RA – real estate

Add one BDC and insurance preferred BHFAP, and you’ve got a shockingly well-balanced 2026–2027 foundation (minus AI/blockchain and consumer sectors).

If you’re new and starting from scratch:

Equal weight 7 of these 10 names and you’ve basically built 70% of a diversified income portfolio.

And yes…

We don’t hold any of them yet.

Pain.

Portfolio Updates

1️⃣ Vanning Portfolio

This week’s cash went into:

- ULTI (adding more)

- GNT (new position)

- Covered-call CEF

- Gold + natural resources exposure

- We plan to keep building this through 2026—as long as the price cooperates.

2️⃣ Retirement Portfolio

This week’s contribution went straight into:

- LYB (adding more on the dip)

Slow, steady, strategic. Exactly how this portfolio is designed to run.

Want Instant Notifications For These Investing IINsights?

We post these updates to several places where you can subscribe and get notified as soon as we post.

- Substack

- LinkedIn Newsletter

- Our email list (no spam, just 1 email a week). Sign up below.