The shutdown delayed a ton of government data, and now the numbers are finally trickling in — and they’re telling a very different story than the headlines. Consumer spending is shifting toward necessities, private jobs are quietly bleeding, and producer prices are creeping up in all the places you don’t want them to.

This is one of those weeks where reading the actual data matters way more than the narrative. So let’s break down what’s real, what’s B.S., and what it means for your money this week.

Economic News

1️⃣ Retail Sales: The Headline Looked Fine — The Details Don’t

We finally got the September retail sales report, delayed thanks to the shutdown. Headline number: retail sales up 0.2% (below expectations).

But digging into the details? Different story. Consumers cut spending on anything that wasn’t essential:

- Sporting goods, books, instruments ↓ 2.5%

- Clothing ↓ 0.7%

- Electronics/appliances ↓ 0.5%

- Online retailers ↓ 0.7%

- Vehicles/parts ↓ 0.3%

Where spending did rise:

- Gas stations ↑ 2%

- Health & personal care ↑ 1.1%

- Food services ↑ 0.7%

- Furniture ↑ 0.6%

- Physical retail stores ↑ 2.9%

Translation:

People are cutting back on wants and sticking to needs — and doing their buying in person. Not as “strong” as the headlines are spinning it.

2️⃣ ADP Report: The Labor Market Is Softening (No Matter What the Regime Says)

ADP private jobs report came in… and yeah, it’s caca.

Private-sector jobs lost an average of 13,500 jobs per week over the past month.

This directly contradicts last week’s government “data” claiming 110,000 new jobs added.

One week ago the losses were only 2,500/week. Now we’re at 13,500/week.

We’ll talk more once the detailed ADP report drops next week, but the trend is clear:

The labor market is weakening, no matter how shiny the official numbers look.

3️⃣ PPI: Producer Prices Are Quietly Rising (Tariff Bleed-Through Begins)

September PPI increased 0.3%, with energy leading the charge:

- Energy prices ↑ 3.5%

- Gasoline alone ↑ 11.8%

Year-over-year producer prices are up 2.9%, well above the 2.0% target.

More concerning: prices rose across all processed goods — food, feed, energy, etc.

This is early evidence of tariffs bleeding into real costs.

Again, this is September data — we’ll need the October report to confirm the trend.

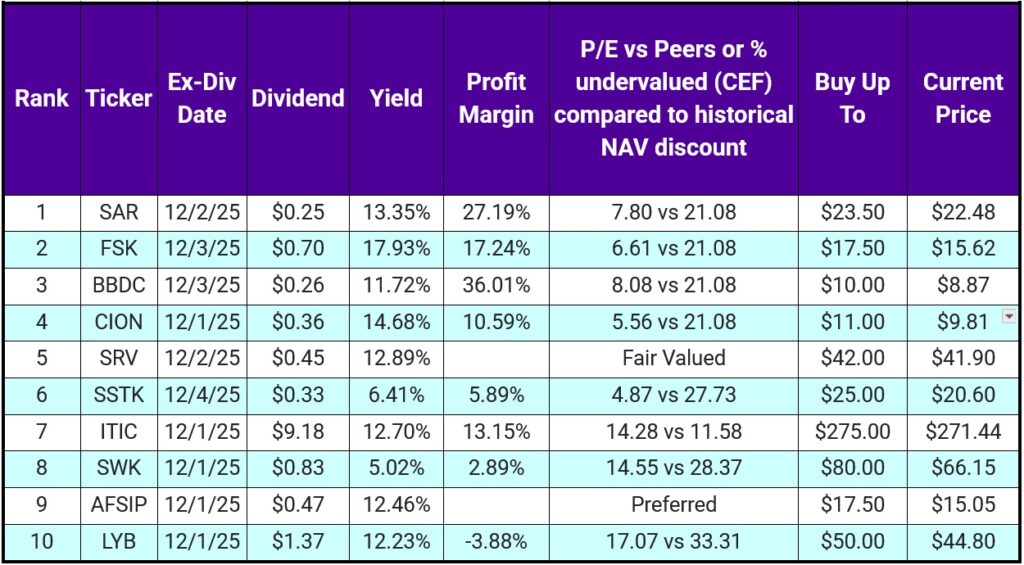

Top 10 IINvestments Going Ex-Dividend Next Week

BDC-palooza this week: SAR, FSK, BBDC & CION.

Quick notes:

- SAR is paying both its regular $0.25 dividend and an additional $0.25 special this month.

- ITIC is paying a regular $0.46 dividend plus a monster $8.72 special dividend — always worth investigating when it’s that large.

The list includes:

- 4 BDCs: SAR, FSK, BBDC, CION

- 1 Oil CEF: SRV

- 1 Tech/Images: SSTK

- 1 Insurance: ITIC

- 1 Power Tools: SWK

- 1 Preferred: AFSIP

- 1 Chemical: LYB

We currently hold FSK, SRV, and LYB across our portfolios.

FSK has had a rough 2025, but if you believe BDCs rebound in 2026 (we do), it’s worth a look.

LYB is tricky — profit margins are hard to nail down and recent data isn’t great. I’d wait for their January earnings before making a move.

Portfolio Updates

1️⃣ Vanning Portfolio

The cash we accumulated this week has been dumped into WPAY. We are slowly building this position.

2️⃣ Retirement Portfolio

The cash this week was dumped into TGT. This position is getting quite nice.

Want Instant Notifications For These Investing IINsights?

We post these updates to several places where you can subscribe and get notified as soon as we post.

- Substack

- LinkedIn Newsletter

- Our email list (no spam, just 1 email a week). Sign up below.