If you’re feeling like the economic headlines aren’t quite matching reality, you’re not wrong. This week’s data shows inflation climbing fast, retail sales getting the ol’ revision rug-pull, and more signs that the economy we’re told we’re in isn’t the one we’re actually experiencing.

Let’s break it down, cut through the noise, and figure out how to stay positioned before the market wakes up and smells the CPI.

Economic News

1️⃣ CPI: Surprise (not really)—Inflation’s Heating Up Again

The June CPI report confirmed what we’ve been warning about for weeks: inflation’s not under control. Prices rose 0.3% in June. Core inflation is 2.9% year-over-year, non-core sits at 2.7%. And this is just the warm-up.

Thanks to tariffs, consumer costs will keep rising—tariff receipts jumped $29 billion in June alone. Spoiler: those costs don’t magically vanish—they get passed to us. So we’re sending billions more to Uncle Sam, who’s spending it on ICE, defense, and tax cuts for millionaires. Super cool.

Here’s the most alarming part:

- Energy up 1.9%

- Gasoline up 3.6%

- Airfare up 2.6%

- Meat up 1.1%

- Instant coffee up 5.6%

- Apparel up 0.8%

These were the categories that had been keeping CPI numbers lower. That’s over. We’re now staring down the barrel of 4%+ inflation unless something drastic changes.

If that happens, the rate cut markets have priced in for 2025? Dead on arrival. If anything, the Fed might need to raise rates again. Wrap your head around that reality.

2️⃣ Retail Sales: The Data That Lies with a Smile

On the surface, June retail sales were up 0.6%. Cool, right? Except… May was down 0.9%, and the actual numbers tell a different story.

The raw data shows that almost every category except “Sporting goods & bookstores” declined. The “growth” is entirely from adjusted data—which doesn’t account for actual price increases, just seasonal fluff.

Example:

- May 2025 retail sales were initially reported at $753B

- Actual number just released? $715B

A $38B “adjustment.” That’s over 5%, y’all. This is why trusting government data—at face value—is risky. It’s always spun to fit a narrative, and right now that narrative is “the consumer is strong.” Sure. OK.

3️⃣ Labor Market: Some Light, But the Wall Is Coming

Jobless claims fell by 7,000 to 221,000, a decent sign that parts of the labor market are still holding up. But don’t get too comfy—private sector weakness has been building for weeks, and this resilience might just be the final flicker before it breaks.

We’re calling it now: Jobs will be the last domino to fall in the tariff + inflation chain reaction.

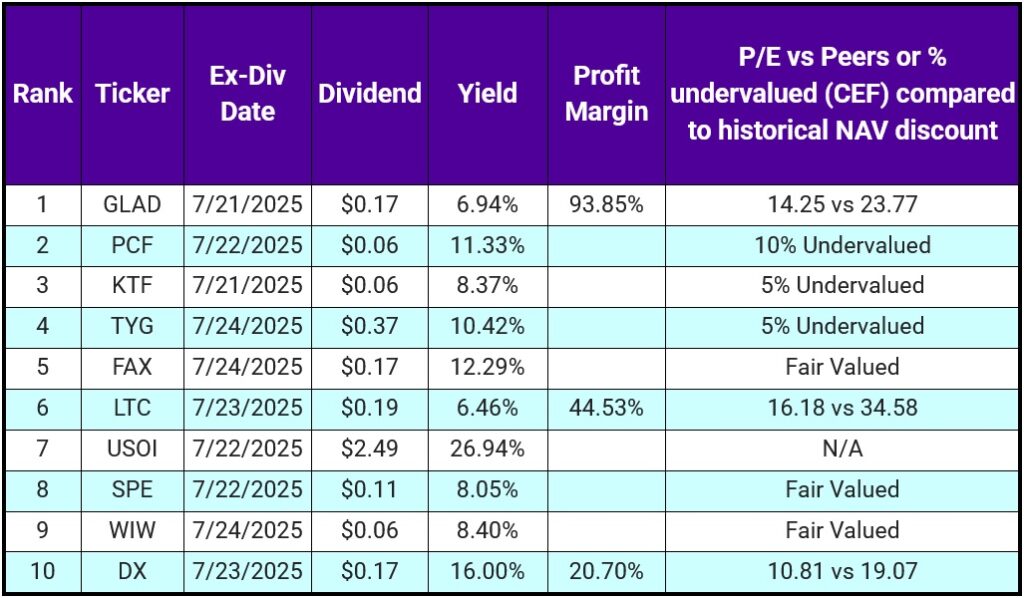

Top 10 IINvestments Going Ex-Dividend Next Week

Solid mix this week—doesn’t matter what direction the market goes, there’s something to work with here.

Sectors represented:

- BDC: GLAD

- Mortgage REIT: DX

- Healthcare REIT: LTC

- Muni Bonds: KTF

- Emerging Markets: FAX

- Inflation Protection: WIW

- Energy: TYG

- Oil & Commodities: USOI

We currently hold: SPE, WIW

We’ve previously held: LTC, GLAD, DX, USOI

It’s rare to get this much diversification in a single ex-div week. A few of these are undervalued and could shine in a volatile environment.

Portfolio Updates

1️⃣ Cash Rotations Continue

Nothing flashy this week. We’re still deploying cash into LFGY, OZK, and SPMC—our go-to value plays right now.

2️⃣ Coke, ADM, and the Corn Syrup Crisis?

The Overlord announced that Coke is switching U.S. production to cane sugar (like Mexican Coke), which could be a big hit for ADM—one of the largest producers of high fructose corn syrup.

This isn’t confirmed by Coca-Cola yet, but if it goes through, ADM’s margins and profits could drop hard. Worth watching closely. Could create a buy opportunity—or a reason to cut bait.

That’s a wrap.

Want Instant Notifications For These Investing IINsights?

We post these updates to several places where you can subscribe and get notified as soon as we post.

- Substack

- LinkedIn Newsletter

- Our email list (no spam, just 1 email a week). Sign up below.