Another week, another episode of “America’s Got Shutdowns.” The government’s still dark, the politicians are still pointing fingers, and the economic data is about as scarce as common sense in D.C. But that doesn’t mean the markets stop moving. Prices are climbing, fear is spreading, and everyone’s suddenly acting like gold’s the answer to everything. Spoiler alert: it’s not.

Let’s dig into what’s really going on, why the “safe havens” aren’t so safe, and how we’re positioning our portfolios while the headlines burn.

Economic News

1️⃣ The Government Shutdown Continues

Well, here we are again. The government shutdown is now the second longest on record—and there’s still no end in sight. Normally, I couldn’t give a cat’s furry ass about political theater, but this one’s starting to sting economically.

Federal workers without paychecks = less spending, more unemployment, and frozen contracts that ripple through businesses here and abroad. If the Overlord actually follows through on his “no pay” or “you’re fired” threats, buckle up. It’s going to get messy before it gets better.

2️⃣ Fashion’s 2025 Inflation Runway

AlixPartners released a study on 9,000 shoppers and confirmed what we’ve been saying for months—tariffs = higher prices.

Across all nine categories of fashion (tops, bottoms, outerwear, etc.), prices are up an average of 17% in 2025 compared to 2024.

- Outerwear leads with a 24% spike.

- Swimwear’s the “winner” at only 2%.

Not exactly shocking, but it does highlight how widespread price inflation has become—even in discretionary sectors like fashion.

3️⃣ The Gold Mirage

Every now and then, someone asks why we don’t have exposure to gold or silver. Short answer: math and logic.

Here’s the breakdown:

- The “inflation hedge” myth:

Over the past 30 years, gold’s annual return averaged 2.9%. Inflation? Between 2.9% and 3.3%.

Translation: you broke even before fees. - Fees eat your profits alive:

- Storage: 0.5–1%

- Insurance: 1–2%

Even at the low end, that’s a 1.5–3% loss every year.

- Taxed worse than stocks:

If you’re in a higher bracket, you pay 8% more in taxes on gold profits than on stock profits. - No income, no edge:

Over the past decade, stocks beat gold by ~4% without even counting dividends. With stocks, you actually get paid to wait.

So, yeah. I’ll stick with cash-flowing assets that beat inflation and pay me to own them.

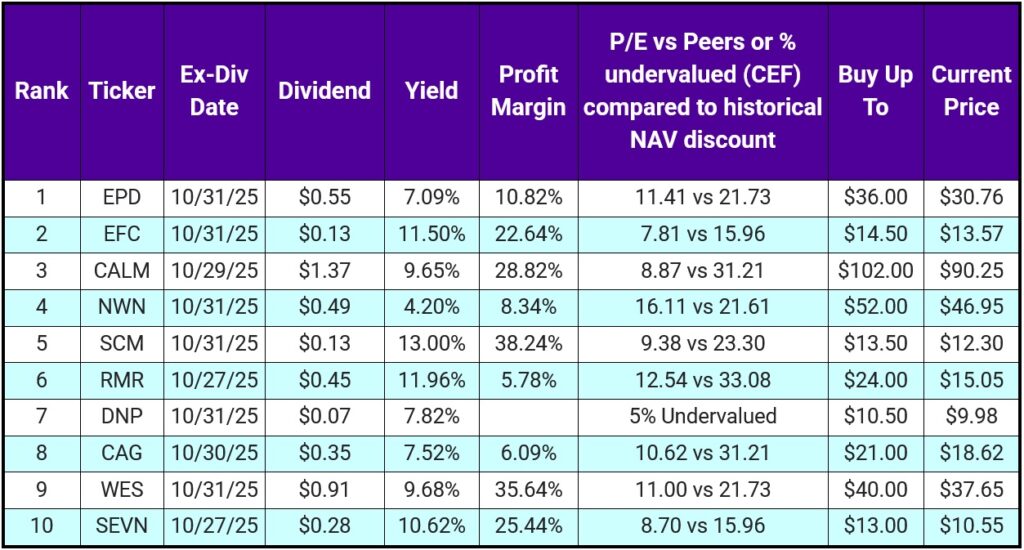

Top 10 IINvestments Going Ex-Dividend Next Week

After last week’s sub par list, this week’s lineup is 🔥. Every one of these 10 could make you bank.

Here’s what we’ve got:

- 🛢️ 2 midstream oil plays: EPD & WES

- 🏠 2 mREITs: EFC & SEVN

- 🍳 2 food stocks: CALM & CAG

- 🔌 1 gas utility: NWN

- 💼 1 BDC: SCM

- 🏢 1 REIT: RMR

- ⚡ 1 utility CEF: DNP

They’re all fairly valued with solid yields.

⚠️ Note on CALM: Variable dividend payer. Dividends over the past two years have swung from $0.12 to $3.50 per share. Great if you can handle the variance—not great if you need steady income.

We currently hold EPD, and I absolutely love it. While crude oil has dropped nearly 20% YTD, EPD is only down 1.6% (or up 3% if you include dividends).

This is exactly why I prefer midstream plays over big oil names like Exxon or Chevron—they get paid for transporting and storing oil, not betting on price swings.

IMO, crude oil is one of the most manipulated assets on the planet. It should be around $150/barrel, but thanks to OPEC and political meddling (hi again, Overlord), we’re sitting at ~$58.

Portfolio Updates

1️⃣ RYLD → Gone

This one hurts a bit. RYLD was our second-longest holding (5+ years) and 2nd investment I placed in this portfolio, but it’s been dead money. Small caps have ripped, RYLD hasn’t. Plus with recent pull backs I can use these funds elsewhere to get more money flow. We sold at a yucky 5% loss, but that freed up $2,400 that was only making $23/month.

2️⃣ RYLD Proceeds Reallocation

With the RYLD proceeds, we bought:

- QQQI, SPMC, FSK, THTA, and MSTY

- Plus, we opened a new position in BMY (one of my decade-long conviction plays).

At $43.50–$44.00, BMY is an absolute steal. It’s a 5%+ yielder with 18 consecutive years of dividend raises, a dirt-cheap P/E of 6.79, and a PEG ratio of 0.239. It’s currently out of favor because of political noise impacting free cash flow, but the fundamentals are rock solid. EPS keeps beating estimates, revenue’s trending upward, and analysts peg a 13.6–29.5% upside over the next 12 months (target range $50–$57). For us, anything under $47 is a greenlight buy.

This round of repositioning increases our monthly income from $24 to $36, adds $23 quarterly from FSK, and gets our BMY compounding machine started. It’s not flashy—it’s tactical, and it’s how you make progress when you’re working with limited capital: one efficient, high-yielding move at a time.

3️⃣ RWAY → Sold

Another bittersweet goodbye in the vanning portfolio. We sold all shares of RWAY. Selling a 14% yielder is always tough, but I wanted the cash in other things. We held RWAY for almost a year and exited the position with a 10% gain.

4️⃣ RWAY Proceeds Reallocation

With those proceeds, we bought:

- 38 more THTA

- 10 more UPS

- 15 more BMY

We traded a 14% yielder for three positions yielding ~8.5% combined. Slight dip in yield, but a big boost in quality.

5️⃣ Cash Allocations

In the retirement portfolio we used the cash we collected over the past week to buy more LTC and TGT shares.

Want Instant Notifications For These Investing IINsights?

We post these updates to several places where you can subscribe and get notified as soon as we post.

- Substack

- LinkedIn Newsletter

- Our email list (no spam, just 1 email a week). Sign up below.