If you only read headlines this week, you’d think the economy is cruising, inflation is under control, and rate cuts mean smooth sailing ahead.

If you actually look at the data?

Consumers are quietly tapping out, jobless claims just jumped hard, and the Fed basically admitted inflation isn’t going anywhere for years.

This week’s numbers continue a trend we’ve been calling out for months:

people are spending more on what they need and cutting back hard on what they want. That’s not confidence — that’s survival math.

Let’s get into it.

Economic News

1️⃣ PCE Report: Not “Bad”… But Also Not Good

September’s PCE report dropped, and on the surface it didn’t look awful:

- +0.3% for all goods

- +0.2% excluding food and energy

- +2.8% YoY inflation

The “experts” were expecting worse, so naturally this got spun as a win.

But once you dig into the spending data, the story changes fast.

Where consumers spent MORE month-over-month:

- +$17.2B on gas & energy

- +$15.4B on housing & utilities

- +$12.6B on health care

- +$12.5B on financial services & insurance

- +$8.2B on food & food services

Where consumers spent LESS:

- –$7.4B on motor vehicles & parts

- –$6.3B on recreational goods & vehicles

- –$3.8B on clothing & footwear

- –$1.9B on other durable goods

This is now the third report in a row showing the same pivot:

👉 discretionary spending down, essential spending up.

That means one of two things:

- People are scared and saving

- Or essentials cost so much there’s nothing left for anything else

Neither scenario is bullish.

2️⃣ Home Prices Are Falling (Again)… And That’s Not Great

For the first time in over two years, home prices are lower than they were 12 months ago.

- Buying today costs about 1% less than December 2024

- Yay? I guess?

Last time this happened (2023), mortgage rates jumped from ~4% to over 7% in a few months as higher Fed rates finally filtered through.

So why is this happening now with rates supposedly falling?

Because:

- The labor market has softened significantly

- Prices for everything else have accelerated

- Mortgage rates are still ~6%

- Inventory is tight

- Demand is weak

This is less about housing and more about what housing reflects:

a consumer who doesn’t feel stable enough to take on a massive loan.

Keep your peepers peeled — housing is a lagging indicator, and this isn’t comforting.

3️⃣ Another Rate Cut… and a Very Honest Admission

In the shock of absolutely no one, the Fed cut rates another 0.25%, putting the Fed Funds range at 3.5–3.75%.

But the press conference is where things got interesting.

The Fed:

- Signaled 1 cut in 2026

- 1 cut in 2027

- Admitted inflation will stay above 2% until at least 2028

Translation:

The Fed is more worried about the labor market breaking than inflation staying elevated.

Markets, of course, did market things and ripped higher on what is objectively not great news.

We’ll see how long that celebration lasts.

Jobless Claims: When 2020 Is the Comparison… Yikes

Weekly jobless claims jumped 19% last week.

Anytime your labor data starts getting compared to the 2020 dumpster fire, that’s… not ideal.

To be continued.

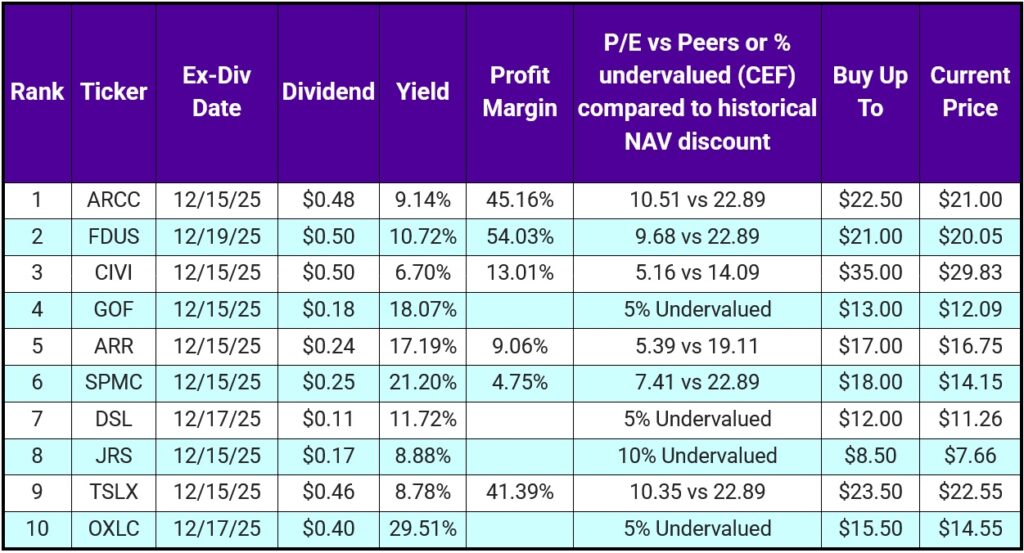

Top 10 IINvestments Going Ex-Dividend Next Week

This week’s list is solid — not amazing, but definitely not trash.

CEFs (4):

- GOF, DSL – bond CEFs

- JRS – REIT CEF

- OXLC – bank loan CEF

BDCs (4):

- ARCC, FDUS, SPMC, TSLX

Other:

- CIVI – oil exploration

- ARR – mortgage REIT

We currently hold ARCC, CIVI, and SPMC.

If you can grab CIVI under $30, you’re doing much better than we did.

Portfolio Updates

1️⃣ HTGC: Initial Investment Recouped

In the vanning portfolio, HTGC is now officially all profit.

- Trimmed due to exceeding our 5% position threshold

- Still hold 200+ shares, now compounding with DRIP back on

2️⃣ Reallocating HTGC Profits (Risk vs Reward)

We deployed the proceeds into:

- ULTI: ~$29.16/month

- WPAY: ~$19.08/month

- GNT: ~$3.05/month

The HTGC shares sold would’ve paid $33.37 per quarter.

New setup should generate ~$120.50 per quarter — a 361% increase.

⚠️ Risk check:

- HTGC = solid company

- ULTI/WPAY = variable income

- GNT = CEF risk

We’re trading stability for income, knowingly and deliberately.

3️⃣ UAN Position Trimmed

UAN also crossed the 5% threshold, so we trimmed and locked in profits.

4️⃣ New Position: DLR Preferred (DLR-PRL)

Instead of paying $165/share for DLR common:

- 2.96% yield

- ~20% upside forecast

We bought the preferred:

- ~$21/share (~16% discount)

- 6.2% yield

DLR fundamentals:

- Revenue up 42% in 4 years

- ~$17B debt

- ~$6.4B revenue

Same company. Better income and lower price. And hopefully less drama than our QVC preferred ha.

5️⃣ Retirement Portfolio

This week’s retirement cash went into more OZK at attractive prices.

Want Instant Notifications For These Investing IINsights?

We post these updates to several places where you can subscribe and get notified as soon as we post.

- Substack

- LinkedIn Newsletter

- Our email list (no spam, just 1 email a week). Sign up below.