Last week we were staring down a trade war with Europe, markets were spiraling, and everyone was pretending Greenland was suddenly the most important place on Earth. This week? A “framework of a deal” magically appeared, the market sighed in relief, and everyone collectively moved on like nothing happened.

Except consumers didn’t.

Under the surface, the data continues to paint a very different picture—one where confidence is collapsing, prices remain elevated, and the people actually spending money feel like the economy is… not great.

Let’s get into it.

Economic News

1️⃣ Trade War Averted (For Now)

The trade war with the EU was officially not happening anymore after Agent Orange announced a “framework of a deal” giving America access to Greenland.

Here’s the fun part:

So far, that “framework” appears to include everything the U.S. already had access to—military deployments, mineral rights, the whole package. So either this deal has a very exciting second page we haven’t seen yet, or this was mostly a vibes-based announcement to calm markets.

Mission accomplished, I guess.

Markets had a HUGE sigh of relief, which tells you everything you need to know about how fragile sentiment still is. This story isn’t over, and I’d expect Greenland to keep popping up in headlines like an awkward third wheel for months to come.

2️⃣ Consumer Confidence: Yikes on Bikes

The Conference Board Consumer Confidence Survey for January came in… bad. Like historically awkward bad.

- Consumer Confidence Index: down 10%, lowest level since 2014

- Present Situation Index: down 8%

- Expectations Index: down 13%

Apparently COVID and a mini-recession in 2022 were better vibes than now…

Before anyone screams “bias!”—these declines showed up across:

- All age groups

- All income brackets

- All political affiliations

This survey has been around since 1967, so while I do side-eye the online sample size (5,000 households across 9 regions isn’t exactly the entire country), it’s still a meaningful signal.

Here’s the takeaway:

People who shop online and bother filling out surveys are pissed.

Combine this with University of Michigan data and the regime’s “everything is amazing” talking points, and you get a consumer who is:

- Cash-strapped because prices are still high

- Emotionally exhausted from nonstop bad news

If this is the best economy in the history of the United States, consumers apparently missed the memo.

3️⃣ The Fed Held Rates… and Everyone Pretended to Be Surprised

Agent Orange is mad. Very mad. He wants rate cuts at basically every meeting.

The irony?

The same data being used to sell the “best economy ever” narrative is also why rates stayed where they are.

- The Fed says the labor market is stabilizing (questionable if you read the reports).

- The Fed says inflation is elevated but manageable (also questionable if you buy groceries or pay utilities).

Markets are currently pricing in:

- One guaranteed rate cut in 2026

- One additional “maybe” cut

But if data continues to be… let’s call it massaged… rates could stay exactly where they are all year. Strong economy narratives have consequences, and this is one of them.

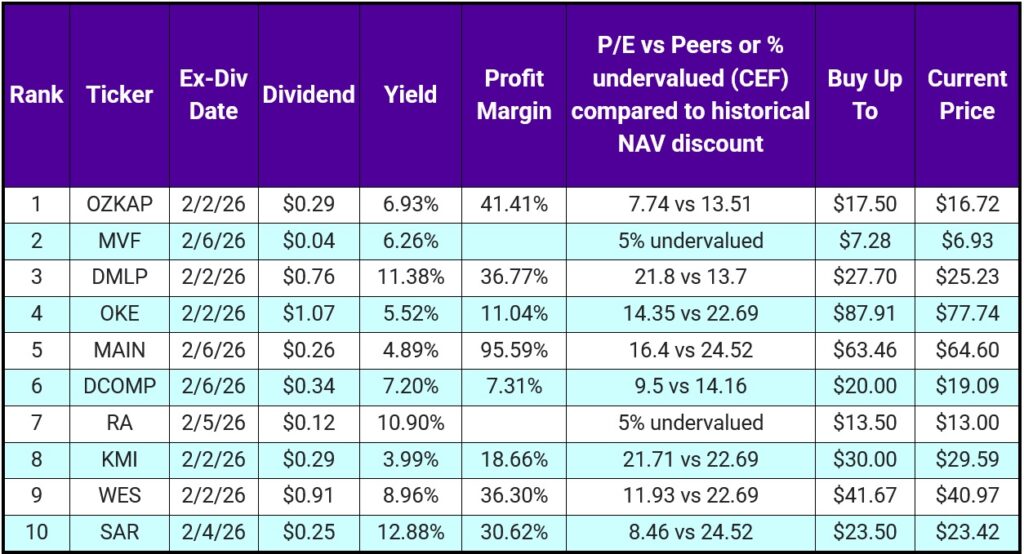

Top 10 IINvestments Going Ex-Dividend Next Week

Full disclosure: we’ve held DMLP, MAIN, RA, and SAR at various points over the past couple of years, so this list isn’t totally foreign territory.

This week’s lineup:

- 3 Energy / Midstream plays: OKE, KMI, WES

- 2 BDCs: MAIN, SAR

- 2 Financial Preferreds: OZKAP, DCOMP

- 1 Mineral Royalty: DMLP

- 1 Real Asset CEF: RA

- 1 Municipal Bond CEF: MVF

Is it perfectly diversified? No.

Did the numbers force our hand? Yes.

We don’t currently hold any of these (though we do hold OZK, so that’s a moral victory). I like the top six for a combination of yield and potential price appreciation. The bottom four? Honestly… could do anything.

If none of these excite you, holding cash is not a failure. Next week should offer a better menu.

Portfolio Updates

1️⃣ New Position

In the vanning portfolio, we used cash this week to initiate a new position:

SEMY

- Weekly payer

- Writes put options on SOXL

- Does not hold underlying stocks (yes, I know—suboptimal)

Why did we still do it?

- Average ROC ~54%

- Three of the last four payouts were 0% ROC

- Semiconductors, historically, tend to be a pretty solid place to make money over time

This is absolutely a flier, not a core holding. We’re watching it closely and will report back if it behaves—or misbehaves.

Want Instant Notifications For These Investing IINsights?

We post these updates to several places where you can subscribe and get notified as soon as we post.

- Substack

- LinkedIn Newsletter

- Our email list (no spam, just 1 email a week). Sign up below.