If you only listened to the headlines this week, you’d think inflation is “cooling” and everything’s fine. But if you actually look under the hood—CPI, PPI, and unemployment data tell a very different story. Spoiler: it’s ugly. Prices are climbing in almost every sector, producers are getting squeezed, and ongoing unemployment claims just hit a 3-year high.

That’s the bad news.

The good news? We’ve been positioning for this. This week’s moves include a healthcare REIT set for double-digit returns, a dividend king trading at a 40% discount, and a Bitcoin-adjacent growth stock that just signed a multi-billion-dollar deal with Google. Let’s get into it.

Economic News

1️⃣ Unemployment Claims: The Silent Alarm

Initial claims: Up just 5,000 (good—means layoffs are still low).

Ongoing claims: Up 38,000 to 1.974M (bad—people who lose jobs aren’t finding new ones).

Why it matters: This is the “stickiness” metric. The harder it is to get rehired, the more the economy slows. Keep an eye on this one.

2️⃣ CPI – The Pretty Lie (and a BLS caveat)

Not that we can trust anything the Bureau of Labor Statistics reports anymore since the Overlord fired the head statistician he disagreed with over last week’s jobs data, but here goes…

- Headline CPI: +0.2% in July, +2.7% YoY.

- Core CPI (ex-food & energy): +3.1% YoY—still well above the Fed’s 2% target.

Under the hood, June → July jumps include:

- Dairy +0.7% (YoY +5.2%)

- Motor fuel +1.8%

- Medical care +0.8%

- Vehicle maintenance +1.0% (YoY +6.5%)

- Airline fares +4%

14 of 15 categories (ex-food & energy) rose month over month. Energy softness is the only thing masking how bad this report is.

So don’t listen to the people who have a narrative to push—prices are going up, and it’s because of tariffs. Without the negative drag from energy and oil, this would be a disaster print. But sure, we’ll all get to hear how “great” the economy is all day and the rest of the week.

3️⃣ PPI – The Inflation Crystal Ball

The Producer Price Index (PPI) is basically what producers pay before passing costs on to you, the consumer. And when producer costs jump, consumer prices almost always follow. Many “experts” use the PPI as an early indicator for where the CPI is headed.

For July:

- PPI: +0.9% MoM, +3.3% YoY

- All major sectors up, and some are up big:

- Final demand foods +1.4%

- Final demand energy +0.9%

- Final demand trade +2.0%

- Processed goods +0.8%

- Unprocessed goods +1.8%

- Stage 1 production flow +1.1%

- Stage 4 production flow +0.8%

This is just the increase from June → July, and it’s almost like a crystal ball showing higher consumer prices in the near future.

As soon as this report dropped, the market fell 1% on the spot. So here’s where we are:

- CPI is already rising, but “experts” keep saying it’s not that bad.

- PPI is outright awful and getting worse.

Yeah, those pundits claiming tariffs aren’t causing inflation are frankly full of shit. Be prepared for prices to go up and the stock market to go down—the data says so.

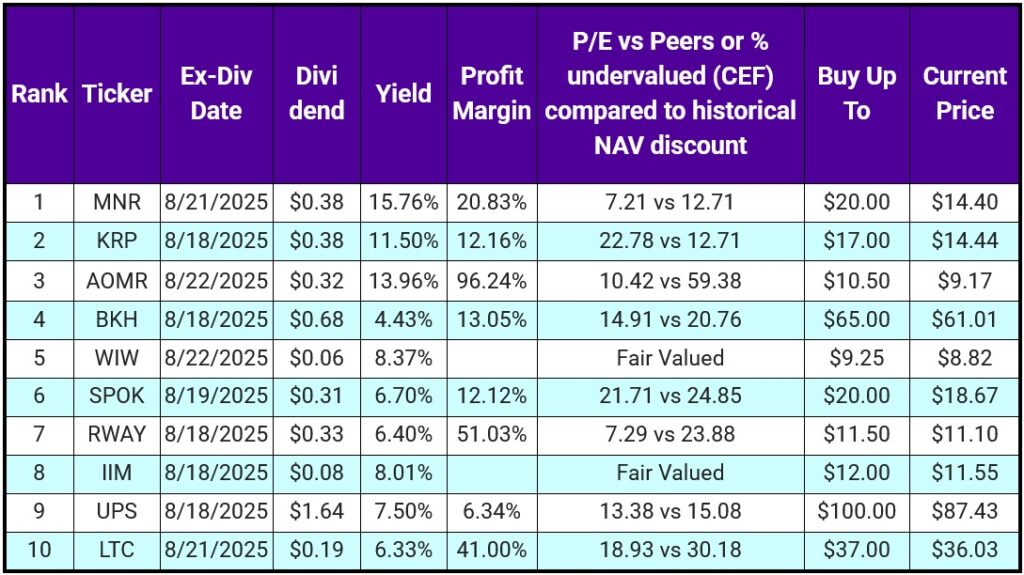

Top 10 IINvestments Going Ex-Dividend Next Week

Trying something new with the chart this week. Figure what’s the point of giving the data if you don’t know the buy-up-to point. If you hate it, I’ll go back to the old chart.

Not the juiciest yields this time (happens when you stick to the metrics), but the diversification here is solid: oil, mineral royalties, BDCs, utilities, inflation protection, healthcare comms, healthcare REITs, and even UPS.

Our holdings from this list: MNR, KRP, BKH, WIW, RWAY, UPS, LTC.

Most intriguing this week: AOMR (BDC) and SPOK (healthcare comms). I’ll probably throw some clams at both soon.

Portfolio Updates

1️⃣ Initiated Position in LTC (Healthcare REIT)

We put our free cash in the retirement account to work by opening a position in LTC Properties—and yes, I’m hoping it performs better than our MPW adventure.

Here’s the thinking:

- Demographics are destiny — 10,000 Boomers retire every single day, which means healthcare real estate is going to stay in high demand for decades.

- Numbers check out — $0.19 monthly dividend (6.5% yield), Q2 NII at $0.32 (a bit light), but FFO came in strong at $0.68. Revenue grew 20% YoY to $60.2M.

- Growth outlook — NII projected to grow 1–2% for the rest of 2025.

- Valuation — Net profit margins of 41% and a P/E of 19.35 versus a sector average of 30.61 means LTC is undervalued.

- Price targets — “Experts” are calling $37.50 (5% upside), but I think that’s low. My 12–24 month target is $40, which would put 12-month total return potential at 11–15%, and 24-month potential at 25–30%.

This is a defensive, income-focused position that also has room for capital appreciation—exactly what we want in the retirement portfolio right now.

2️⃣ Goodbye EQX, Hello TGT

We rang the register on EQX, our gold mining play we picked up a few years back at $2.50/share. The company was eventually acquired, and we just sold at $6.40—a sweet +156% return.

With those funds, we’re starting a position in Target (TGT) that we plan to build over time. Now, let me be crystal clear: I personally can’t stand Target. But personal feelings don’t pay the bills—valuations do. And right now, TGT is a no-brainer value setup for the retirement portfolio.

Here’s the case:

- Down 22% YTD — This is exactly the type of oversold, blue-chip opportunity we want to pounce on.

- Catalyst incoming — Earnings drop on 8/20, and the bar is so low that beating expectations is highly likely.

- Financial health — Debt has decreased for 3 straight quarters.

- Mixed performance — Revenue was down slightly in Q1 2025 vs Q1 2024, but earnings, EPS, and expenses all improved YoY. Margins and revenue took a hit due to reduced sales and foot traffic.

- The “woke” backlash factor — TGT angered a chunk of its customer base with some advertising campaigns. They’ve since walked back some of it, and we’ll see in the 8/20 report if shoppers are returning.

- Dividend powerhouse — Raised its dividend to $1.14 this year, marking its 54th consecutive annual increase. That’s Dividend King status.

- Valuation disconnect — This is a stock that should be trading between $180–$200 but is sitting at $105.

Bottom line: This is the kind of opportunity where we buy while it’s unpopular, collect a reliable dividend, and wait for sentiment and price to recover.

3️⃣ WULF — The Whim Growth Play That Might Go Big

Sometimes you buy a stock because the ticker is cool (SAGS factor), and sometimes it actually turns into a legitimate winner. WULF checks both boxes.

Here’s the rundown:

- What they do: WULF builds zero-carbon data centers, mostly for Bitcoin mining operations.

- The big news: They just signed two massive contracts with Fluidstack—backed by none other than Google. When finalized, Google will own 8% of WULF stock.

- Deal size: 10-year agreement worth $3.7B–$8.7B depending on extensions. For context, WULF’s current annual revenue is under $200M—so this could double yearly revenue almost overnight.

- Strategic impact: This deal takes WULF from “obscure Bitcoin infrastructure play” to “serious tech infrastructure contender.” And my gut says this won’t be their last major contract.

- Our plan: Any dip under $7 is a buying opportunity. We originally targeted $20 for a sell, but with this new data, $40 feels more realistic.

This one started out as a fun flyer, but it’s shaping up to be one of those investments that might end up paying for our next adventure. #winning

Want Instant Notifications For These Investing IINsights?

We post these updates to several places where you can subscribe and get notified as soon as we post.

- Substack

- LinkedIn Newsletter

- Our email list (no spam, just 1 email a week). Sign up below.