You’re going to hear a lot of cheering about the 3% GDP print this week. Don’t join the parade just yet. That number hides more than it reveals—and if you’re not paying attention to the details, your portfolio will feel it. This week, we break down what actually happened with the economy, what’s coming next, and how we’re positioning to stay ahead of the noise.

Economic News

1️⃣ GDP Q2 = 3%. Big number. Bigger asterisk.

As we predicted, GDP came in strong—but most of the boost came from a massive 30% decline in imports. That’s right: companies front-loaded inventory before tariffs hit, then stopped buying. Exports declined 2%. And while consumer spending technically rose 1.4%, that number is almost certainly just inflation baked in—people paid more and got less.

2️⃣ The Fed held steady—and good

The Fed left rates unchanged despite political pressure. Anyone begging for cuts right now is waving a red flag. There is no data-driven case for easing. For once, the Fed did the right thing. (Gross to say, I know.)

3️⃣ PCE inflation rose 0.3% in June (2.8% YOY)

This confirms what we’ve been saying: inflation is not under control. Yet the market is still pricing in a September rate cut. If inflation stays sticky, and the Fed doesn’t cut? Expect a 5–10% market dip in September. Be ready.

4️⃣ ADP Jobs Report: Solid-ish, but shows slowdown.

May’s job gains were revised down by 30%. July added 104,000 private jobs—decent, but below the 10-year average of 198,000 for the month. Nearly all gains came from the service sector. Translation: The labor market is softening. Slowly.

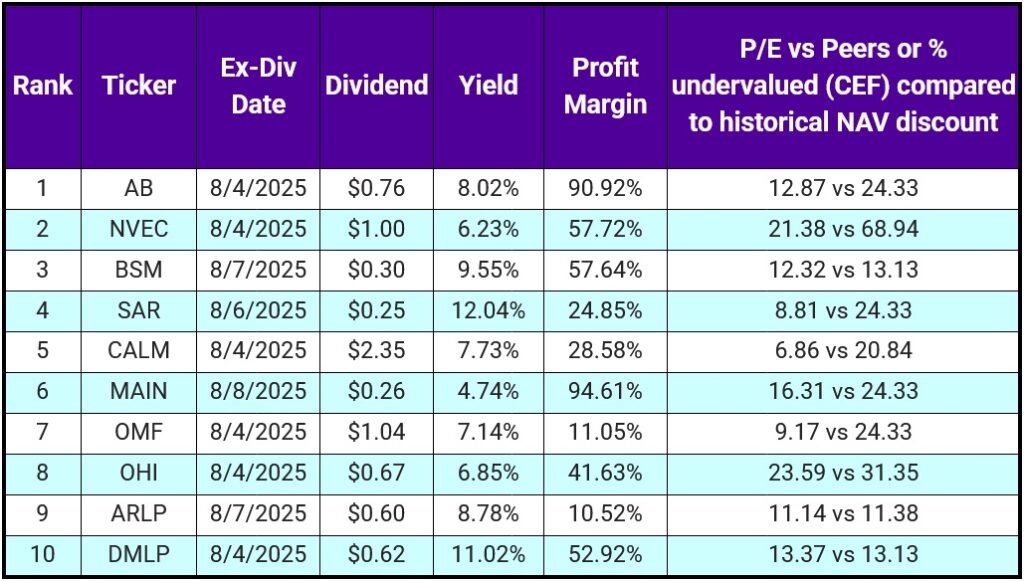

Top 10 IINvestments Going Ex-Dividend Next Week

This list might be our best retirement account lineup yet. Solid, diversified, and built for long-term wealth—without huge risks.

We currently hold BSM, AB, ARLP and have previously held CALM and MAIN. A few highlights:

- NVEC is the wild card. Spintronics play in semis. Nanotech nerd bait. I’ll likely be buying.

- MAIN is a long-term BDC winner, but a little overvalued here. Ideally, buy around a 5.5–6% yield.

- AB & OMF offer more appreciation upside and almost double the yield.

- CALM is an absolute earnings machine. Big regret selling.

- ARLP (coal) just cut its div from $0.70 to $0.60, but still strong.

- DMLP & BSM are royalty plays—low-risk ways to earn off energy/mining without operational exposure.

- OHI is what MPW should’ve been. REIT with real staying power in medical. Aging population = tailwind.

- NVEC is the wild card. Spintronics play in semis. Nanotech nerd bait. I’ll likely be buying.

Portfolio Updates

1️⃣ Took profits in SOFI

In the retirement account, we sold enough to recoup our initial investment. The 54 shares left are pure profit.

2️⃣ Bought CMG on the dip

Used SOFI profits to initiate a position after a 16% post-earnings drop. No dividend, but CMG is down 25% YTD and has strong long-term upside. EPS +17%, revenue +13% projected for 2026. This is a buy-and-hold cap gain play.

3️⃣ Reinvested cashflow into QQQI, MSTY, and NVDW

These are strong monthly and weekly payers. Funded using dividend cash from CONY, YMAX, and USOY.

4️⃣ Strategy Going Forward:

We’re compounding into:

→ QQQI, MSTY, WNTR, and NVDW (targeting $1,000+ positions in each)

→ Cash from CONY, NVDY, JEPQ (all profit)

→ Cash from YMAX, USOY (still reclaiming principal)

To maintain our 60/40 balance (equities vs ETFs/CEFs/cash), we’ll keep adding IIPR and UPS—unless we see a high-conviction equity play, in which case we may liquidate THTA to reallocate.

Want Instant Notifications For These Investing IINsights?

We post these updates to several places where you can subscribe and get notified as soon as we post.

- Substack

- LinkedIn Newsletter

- Our email list (no spam, just 1 email a week). Sign up below.