If you’ve been investing like “the economy is totally fine and nothing weird is happening,” Commerce and the BEA would like a word.

We got a Q4 GDP print that’s basically a speed bump, inflation that’s still not cooperating, and producer prices that are sending the “this will show up in CPI later” bat-signal. Meanwhile oil went from “not bad” to “you’ve got to be kidding me!”

Here’s the data, practical takeaways, and the plays that make sense when the macro gets yucky.

Economic News

1️⃣ Q4 GDP: 0.7% growth (yeah… 0.7)

4th quarter GDP was projected to be in the 1.5%–2% range and instead was reported to be 0.7% growth according to the Commerce Department.

There are some interesting nuggets in the report that point toward being more cautious right now.

First: consumer spending increased 2% compared to Q4 2024, but it shrank hard from 3.5% in Q3 2025.

Here’s how I interpret that: we’re paying more because of tariffs, so the year-over-year increase makes sense. But at the same time, the consumer is clearly spending less, which is what the Q3 to Q4 drop shows.

Second: business investment mirrored consumer spending. Up 2.2% compared to Q4 2024, but down from 3.2% in Q3 2025. AI investment drove business investment in Q3 and Q4, so it’s safe to assume businesses are spending less toward AI now (or at least pulling back from the “throw money at it” phase).

Third: exports fell 3.3% in Q4.

This completely contradicts the narrative behind most of the economic policies being touted by Agent Orange and his peeps. We were sold a bill of sale that said: endure some short-term discomfort on prices for long-term gain down the road. This is the second consecutive GDP report showing exports down a good bit.

And if we aren’t exporting products, there’s no reason for jobs to be created. Which means the “made in America” narrative is shaky at best.

Final point: GDP grew 2.8% in 2024—you know, the awful and icky Sleepy Joe economy Agent Orange was going to trounce. GDP in Agent Orange’s first year grew 2.1%.

None of this should surprise you because we’ve been laying the data out each week. Hopefully you fully embraced that 2025 and now 2026 are years when dividend growth stocks are the logical, safe, risk-mitigation play.

2️⃣ January PCE: inflation up again and oil wasn’t even the problem yet…

The January PCE inflation report dropped the same day as the awful GDP report.

This report was delayed because of the shutdown… or if you’re a conspiracy theory kind of person, until we had other news to distract from how bad the data is.

Inflation in January rose 0.4% from December and sits at 3.1% YoY.

The reason this number is not higher is because energy kept it lower. And that’s the issue: oil is now around $100 compared to the $60 range when this data was tabulated.

If this “not war” war lingers longer than a couple weeks or a month, inflation numbers are going to get bonkers. Think 4%, 5%, or even higher.

It’s also important to look at where the money is going in these inflation reports (you all know this by now):

- Spending increased a lot in services: health care, housing & utilities, financial services and insurance

- Spending decreased in goods: motor vehicles and parts, gasoline and other energy goods, clothing and footwear, food, furnishings and household equipment

We are in a service-first, actual-things-last economy now. That makes sense when prices are high. People pay for what they can’t avoid—health care, insurance, rent/mortgage—and skimp on what they can delay.

If prices weren’t high and people had confidence in the economy, you’d see more “stuff” purchased. You don’t.

3️⃣ February PPI: producer inflation went bananas

February Producer Price Index rose at some bonkers rates:

- 0.7% overall

- 0.5% excluding food and energy

- YoY increases remain elevated beyond the 2.0% target at 3.4% overall and 3.9% excluding food and energy

Remember: these are prices that the people who make shit pay before you, the consumer, even enter the pricing equation.

The regime stated that 30% of the February increase was due to fuel prices, which rose 13.9%.

So you know what is probably not a great decision? Starting a “not a war” war in the Middle East that directly increases fuel prices. Just saying.

Worse yet, food was up in February too: 2.4%.

And within food, the worst reading was fresh and dry vegetables which increased a completely insane 48.9% from January.

This report feeds directly into what we’ve been saying for the last 8–9 months: the only reason inflation has stayed under control was depressed energy prices. Safe to say we will see worse reports in the near future as long as oil is hellabonkers overpriced.

Natural gas was up 10.9% and unprocessed energy was up 6.0%. Combine that with fuel and you get a very worrying picture.

Not great when segments of an inflation report say we’re at levels not seen since 2022… back when inflation was 9%–10%.

So now we get the fun game of how Agent Orange and his regime spin this as the best economic news ever reported.

Stay tuned…

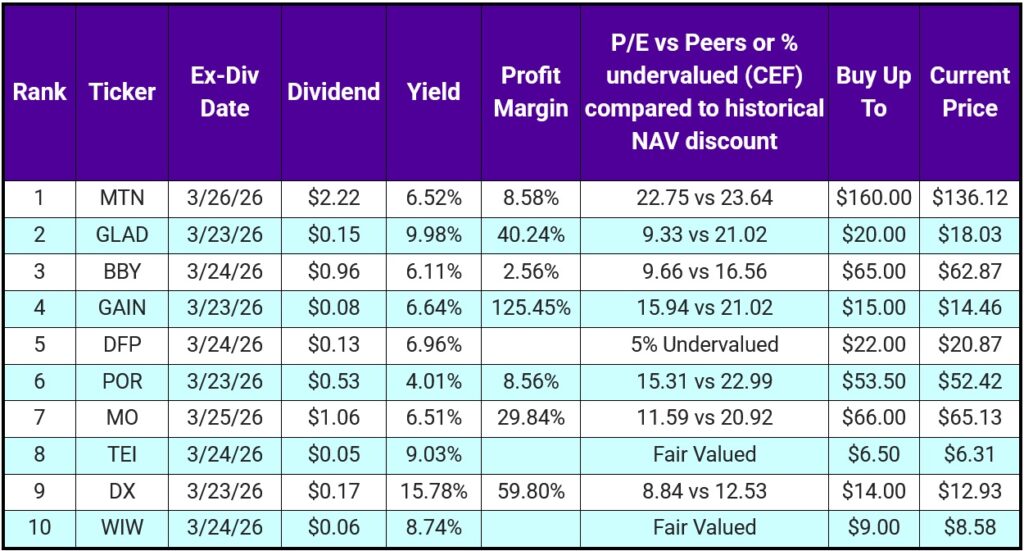

Top 10 IINvestments Going Ex-Dividend Next Week

Before we start: with all the crazy shit going down, prices may or may not be accurate because I’m preparing this on 03/19. Who knows where prices will be by 03/20 when you receive this—just verify prices before buying.

Quite the list this week. There are some good investments to be had. From the bottom:

WIW

WIW is an inflation protection fund. Basically, it trades treasuries to give you a yield above the rate of inflation. If “official” inflation is 3.1%, you need to make sure you’re making more than that in yield or you’re losing money.

An 8.74% yield on a treasury-based fund is a conservative play but keeps you above the inflation line. Getting WIW below $9 should be pretty easy because the price doesn’t fluctuate too much day-to-day. If you’re feeling froggy, wait for $8–$8.25.

DX

DX is a mortgage REIT we hold in the retirement portfolio. I really like mREITs for 2026 and probably 2027.

DX reported NII of $2.49, covering the dividend of $2.00 (81% payout ratio). Margins remain decent. In 2025, DX had a 21.6% return if you combine dividend plus growth in book value.

Book value = total assets minus total liabilities. Think: if the company dissolved today, what would it be worth after selling assets and paying debt? Anything over 1.0 is positive. Anything under 1.0 means it owes more than it owns. DX is currently at 1.03, which is much better than the 0.85 it sat at for most of 2023 into 2024.

TEI

TEI is an emerging market closed-ended bond fund. Monthly dividend + potential for price appreciation.

No way to sugarcoat this: emerging markets are performing much better than U.S. markets. In 2025, emerging markets returned 34% compared to 18% for U.S. markets. In 2026 so far, this trend is continuing—emerging markets up about 7%, U.S. markets down 1%–2%.

If you don’t have emerging market exposure, you’re leaving money on the table. Everyone will choose their own way to do that. For me it’s CEFs: they do the research and work, I collect dividends.

MO

MO should be much higher on this list if not for valuation. 57 years of dividend growth deserves respect. But at current price it’s fair valued at best.

The really messed up part is this: $65 is about fair value, but if you wait for the perfect drop, it may never come. MO is above its 3- and 5-year trailing P/E (overvalued) but below its 3- and 5-year forward P/E (undervalued). So the question is: which do you trust more—trailing or forward?

I bought it below $40 in 2023–2024, so I don’t need to stress. If you’re buying now, I’d wait for $60-ish.

POR

POR is an electrical utility with a 19-year dividend growth streak. Projected 5-year CAGR return of 12% and a fair value estimate around $60 makes this one pretty easy to sleep with at night.

The only thing to consider: POR’s P/E is elevated vs its historical numbers but well below peers. Do you think POR returns to its historical mean? Or do you think it rises toward the utility sector mean P/E? I think it rises toward peers, but that’s my opinion.

DFP

DFP is a preferred stock closed-ended fund that’s undervalued right now. Most preferred shares have a par value of $25, so at $21 this one has room to run. You get about a 7% yield while waiting.

I think the ceiling is around $23–$23.50 for two reasons:

- Active managers often take profits before par

- Historical data suggests it hasn’t lived near $25 since April 2022

GAIN & GLAD

Both Gladstone investments. Both monthly payors. Both can work. The difference is approach:

- GAIN: mix of equity ownership + debt lending

- GLAD: primarily debt lending

Both have around 89% payout ratios right now.

GAIN is at a 4.2% discount to NAV. GLAD is at a 14.7% discount to NAV.

In my honest opinion, GLAD is the better investment. GAIN is closer to fair value. GLAD has more room to run (better price appreciation potential) and you’re getting more than 3% higher yield.

BBY

Best Buy. 22-year dividend growth streak. Dividend growth has slowed (about 2.5% over the past 3 years). Payout ratio is about 34% based on cash flow.

Valuation looks attractive: P/E and P/S are below historical averages, and most “experts” think there’s potential for about 20% price appreciation. Start small, DCA over time, and you’ve got a quality dividend grower.

MTN

MTN’s dividend has exploded out of COVID with a 5-year dividend growth rate above 20% per year. I do think this slows down because the dividend rate is about 140% of earnings—meaning unless earnings improve, the dividend could be cut.

But the reason this is top this week isn’t the $2.22 dividend—it’s valuation. It appears significantly undervalued at $136.

The “experts” average price target is $164–$173, meaning about 30% upside, with a yield above 6%.

Also: mountain resorts are cyclical (winter months are the money months). Insiders are buying this stock on the dip. And insiders usually know the value better than the “experts.” When the CEO and CFO buy $5 million worth of shares, my ears prick up.

Just do your research: MTN has set new 52-week lows 11 times over the past year. High risk, high reward.

And projections for resorts are set to explode at 18.5% CAGR through 2030. I think this is a major sector the “experts” are sleeping on. Again, my opinion.

Portfolio Updates

1️⃣ Vanning main portfolio

We used volatility to our advantage and recouped our initial investment in ARLP. We now have 75 shares that are all profit.

2️⃣ ARLP’s proceeds

With ARLP proceeds, we added 27 shares to NVO and 39 shares to SBAR dry powder.

NVO is still vastly undervalued (48% to 90% depending on your source). I have fair value at $65 right now (76% discounted).

8% EPS growth + 4% dividend + 29-year dividend growth streak + share buybacks = a no brainer anytime you have free cash and NVO is under $40.

3️⃣ Retirement portfolio

Cash in the retirement account was split among SWKS, UPS, and OZK this week.

We picked up 1 share of SWKS, 1 share of UPS, and 3 shares of OZK. Little by little. I know.

Want Instant Notifications For These Investing IINsights?

We post these updates to several places where you can subscribe and get notified as soon as we post.

- Substack

- LinkedIn Newsletter

- Our email list (no spam, just 1 email a week). Sign up below.