You know the drill—grab your coffee (or whiskey, no judgment), because we’ve got another round of government spin vs. actual data to unpack.

Spoiler alert: the numbers don’t lie, even if the “experts” do. Inflation is climbing, sentiment is sinking, jobs are weakening, and yet somehow the markets think we’re all sunshine and rainbows. Let’s dig in and talk about where we’re putting our money instead of hoping and praying.

Economic News

1️⃣ PCE Report: Experts Cheer, Reality Sucks

The July PCE (Personal Consumption Expenditures) just dropped. Wall Street cheered because it “met expectations.” Meanwhile, in the real world, it’s bad: prices rose 0.2% from June to July (0.3% excluding food/energy). Year-over-year, we’re at 2.6%—or 2.9% if you strip food/energy. Both are still above the Fed’s 2% target.

The kicker? Spending is up across the board:

- Motor vehicles & parts: +35%

- Financial services & insurance: +24%

- Housing/utilities: +11%

- Food & beverages: +10%

- Healthcare: +10%

And this “tariffs are a one-off inflation blip” excuse? Total horseshit. If it were one-off, we’d have one or two bad reports, not four straight months of creeping price hikes since April. Call it what it is: a slow, steady bleed of inflation caused by tariffs.

2️⃣ Trade Deficit: The Big Contradiction

The regime keeps telling us tariffs = more U.S. jobs and production. Yet July’s trade deficit widened to $104 billion. Imports hit $281.5B, exports just $178B—a 22% gap. So much for “Made in America.” Tariffs aren’t narrowing the deficit—they’re making it worse. Bravo, Admiral Overlord.

3️⃣ Consumer Sentiment Tanks

This one can’t be manipulated. Sentiment fell 6% from July to August and is down 14.5% YoY. Consumers expect inflation to run 4.8% ove3r the next 12 months. Only 25% plan to maintain big-ticket spending, while personal finance sentiment dropped 7% in a month. Translation: people feel poorer, because they are.

4️⃣ Fed’s No-Win Situation

ADP showed just 54,000 private jobs added in August—weak. The labor market is softening. But inflation is still at 3%. The market, the regime, and the public all want a rate cut in September. Problem: if the Fed cuts, inflation will rise, and jobs still won’t be saved.

We’re sliding into stagflation: low growth + higher prices. Unlike a recession, stagflation drags on for years. Honestly? I’d rather rip the band-aid off with a short recession than suffer through years of this nonsense.

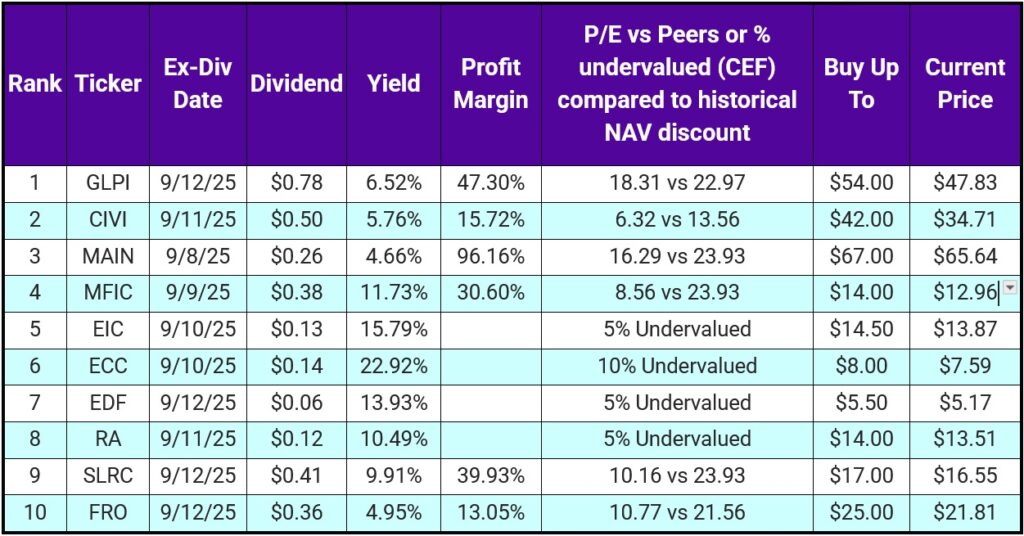

Top 10 IINvestments Going Ex-Dividend Next Week

Finally, a solid list after last week’s trashpanda.

- 4 undervalued CEFs = fat yields (check out EDF + ECC combo: 18.42% yield).

- MAIN is on the list but overvalued IMO—tiny upside isn’t worth a 4.6% yield.

- GLPI is better: ~11% appreciation potential + 6.5% yield.

- CIVI is the only one we currently hold (and yes, this fucker will go up at some point).

We’ve also held MAIN, ECC, EDF, RA, SLRC, and FRO before. I tell you what we’ve owned each week not to brag, but to show you the data drives the decisions—bias doesn’t.

Portfolio Updates

1️⃣ Retirement Portfolio

We added more shares of LTC with available cash.

2️⃣ Vanning Portfolio

We added more shares of PLTW with available cash.

Want Instant Notifications For These Investing IINsights?

We post these updates to several places where you can subscribe and get notified as soon as we post.

- Substack

- LinkedIn Newsletter

- Our email list (no spam, just 1 email a week). Sign up below.