Every week feels like déjà vu: the regime releases data, Wall Street twists it into “good news,” and the Fed dances around with word salads.

Meanwhile, we’re just trying to separate the bullshit from the signals that actually matter to your portfolio. This week? Jobs sucked, inflation ticked higher, and somehow that means champagne for traders. Let’s break it down and then talk about where the real opportunities are.

Economic News

1️⃣ Jobs Report: The Streak Is Dead

The August jobs report landed, and even with the regime’s “massaged” data, it stinks. Only 22,000 jobs were added—ending a 52-month streak of job growth. June’s already pathetic 14,000 gain was revised to a loss of 13,000. Unemployment crept up to 4.3%, the highest in almost four years.

The market? Cheered, of course—because hey, bad jobs = guaranteed rate cuts. Expect a 0.25%–0.50% cut this month. Will that save a weakening economy sliding toward stagflation? Not a chance.

2️⃣ Producer Price Index (PPI): A Fake Holiday

For one brief, shining moment, the headlines screamed “Good News!” because producer prices fell 0.1% in August. Year-over-year, PPI now sits at 2.6% (or 2.8% excluding pesky energy and food). Cue the confetti, right?

Yeah… no. The celebration didn’t last long.

3️⃣ Consumer Price Index (CPI): Parade Rained On

The very next day, CPI reminded us reality sucks. Consumer prices jumped 0.4% in August, now up 2.9% YOY. Excluding food and energy, still up 0.3% MoM / 3.1% YOY.

Where it hurts:

- Food at home: +0.5%

- Dining out: +0.7%

- Gas: +4.1%

- Airfare: +5.9%

- Used cars: +1.0%

- Shelter: +0.2%

- Dental care: +0.7%

The few drops? Medical care (-0.9%) and piped gas (-0.7%).

This report reflects what everyone already feels: 95% of stuff costs more. And with the Fed set to cut rates, don’t be shocked if inflation finishes the year closer to 4%.

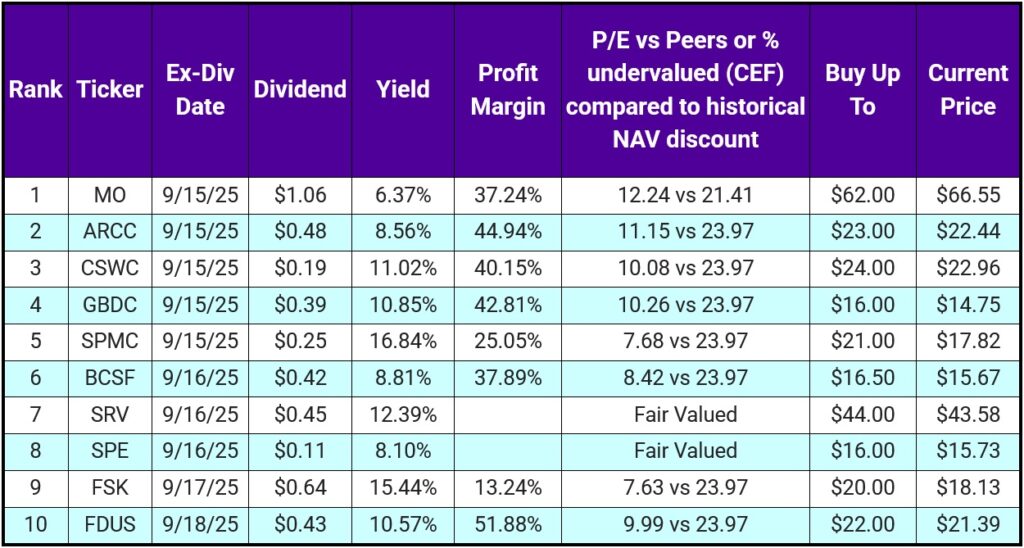

Top 10 IINvestments Going Ex-Dividend Next Week

Finally, a decent list after weeks of trash. Yes, it’s BDC-heavy (7 of 10), but if the Fed cuts rates, BDCs should benefit.

- Star of the list: MO. 50+ years of dividend raises, strong margins. Overvalued right now, but a buy under $70.

- ARCC. The largest BDC by assets, and one I like despite its size.

- CEF caveat. SRV & SPE are fair-to-slightly-overvalued (1–2%), but SRV’s 12% yield covers the risk.

We currently hold MO, ARCC, SPMC, SRV, and FSK. We’ve also held CSWC, SPE, and FDUS in the past. Bottom line: finally a reasonable set of ex-div plays worth your time.

Portfolio Updates

1️⃣ Retirement Portfolio

Added more TGT shares. Still scooping while it’s under $100.

2️⃣ Vanning Portfolio

Added more PLTW shares. Building it out chunk by chunk.

Want Instant Notifications For These Investing IINsights?

We post these updates to several places where you can subscribe and get notified as soon as we post.

- Substack

- LinkedIn Newsletter

- Our email list (no spam, just 1 email a week). Sign up below.