If you’ve been staring at headlines like, “Best economy in the world!” while your wallet makes sad trombone noises… you are not crazy.

This week’s theme is Narrative vs. Numbers — and the numbers are doing that thing where they show up late, slightly drunk, and then change their story in the morning.

Holiday retail sales? → Flat.

Jobs report? → Shiny headline.

Revisions? → The real plot twist.

Anyway… let’s do what we do: ignore the cheerleading, read the fine print, and keep building portfolios that don’t require government press conferences to make sense.

Economic News

1️⃣ Retail Sales: “Best Economy!” Meets… 0%

Another week, another report that shows the dumpster fire that is the data coming from Agent Orange and his regime.

This week’s nonsense: the spin on an ugly December retail report. Holiday sales were projected to be outstanding… and then the actual data showed retail sales for December were flat — and by flat I mean 0% growth over November. Not the projected +0.4% to +0.6%. Just… nothing. Like a New Year’s resolution by February.

It gets better (worse). November was revised downward too: “core” sales (gasoline, building materials, and food) were revised down 50% from 0.4% to 0.2%. Then in December, core retail sales were down 0.1%.

For 2025, retail sales increased 2.4%, which is below inflation (2.7%), meaning people are buying less. This will roll into GDP whenever that drops.

Stay tuned for the next round of “everything is amazing” narration.

2️⃣ Jobs Report: Shiny Object, Meet the Revision Baseball Bat

Okay—this one deserves slow claps. The January jobs report was a masterclass in “lookie at this fun shiny object and ignore everything else.”

Headline:

130,000 jobs added in January and unemployment down to 4.3%. If you believe the data, that’s genuinely solid.

But here’s the “ignore everything else” part:

With revised data, 2025 only added 181,000 jobs for the entire year.

And if you remember, the December report originally said 584,000 jobs for the year. So… yes. That’s a massive revision — about a 70% haircut.

So here we are again: compromised data, markets applauding, and the regime pumping the “cut rates!” narrative.

I’m sure this will be the story that keeps on giving in 2026. Grab the popcorn.

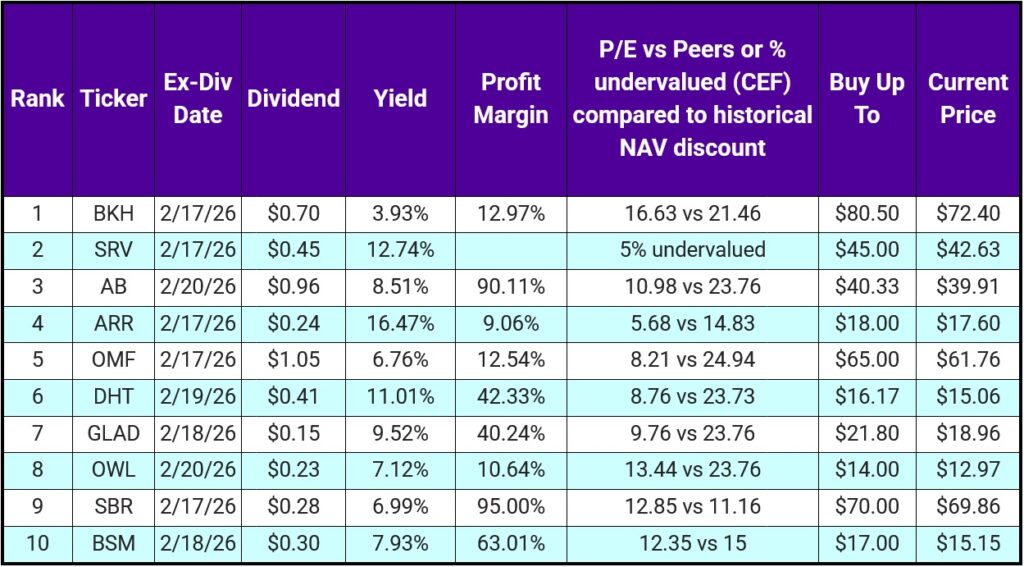

Top 10 IINvestments Going Ex-Dividend Next Week

If you saved cash because last week’s list wasn’t your vibe, this week looks more promising.

Let’s start at the bottom:

BSM – Mineral & mining royalty company with a variable dividend. Not ideal for income-reliant portfolios, but if you can handle quarterly changes, it’s worth a look.

SBR – Oil & gas royalty company with a variable monthly dividend. So you lose consistency, but you get two extra payments each quarter.

OWL / GLAD / AB – All “financials,” but totally different animals:

- OWL = global alternative asset manager

- GLAD = BDC

- AB = investment manager

DHT – Crude oil tanker play that pays out 100% of net income. Great years = great dividends. Lean years = smaller checks.

OMF – 6-year dividend growth streak, decent yield, and it specializes in loans (normally my love language). BUT… defaults are rising, so do your homework. They project delinquency rates rising from 5.85% to 7.4%–7.9% by end of 2026.

ARR – An mREIT with no qualms about cutting dividends. Last cut was Dec 2023 (-42%). It has stabilized and paid $0.24/month since, but… proceed with eyes open.

SRV – CEF holding energy + utilities. Energy is 66% of the portfolio and utilities about 17%. It’s paid $0.45/month since the 2020 cut (which was due to a stock split, not financial issues). SRV has been fairly reliable.

BKH – 56 straight years of dividend raises and projected 6% earnings growth in 2026. Main thing to watch: the NWE merger expected to finalize late 2026. Mergers can cause irrational price drops, so don’t panic if the market gets dramatic.

✅ We currently hold: BKH, SRV, AB, and BSM.

Portfolio Updates

1️⃣ Retirement Portfolio

We added SWKS (3 shares). It’s still undervalued by about 10%, so we keep nibbling and DCA’ing.

2️⃣ Vanning Portfolio: BDC Rotation

We added DLR/PRL (2 shares) and SBAR (12 shares).

DLR/PRL is still about 20% undervalued, and IMO it’s about as close as I can get to a preferred share eventually going back to $25.

SBAR & THTA are our “park cash and wait for violence in the market” funds. Right now we’ve got 1,400 shares of SBAR and 1,915 shares of THTA compounding as dry powder while we wait for awesome deals.

Want Instant Notifications For These Investing IINsights?

We post these updates to several places where you can subscribe and get notified as soon as we post.

- Substack

- LinkedIn Newsletter

- Our email list (no spam, just 1 email a week). Sign up below.